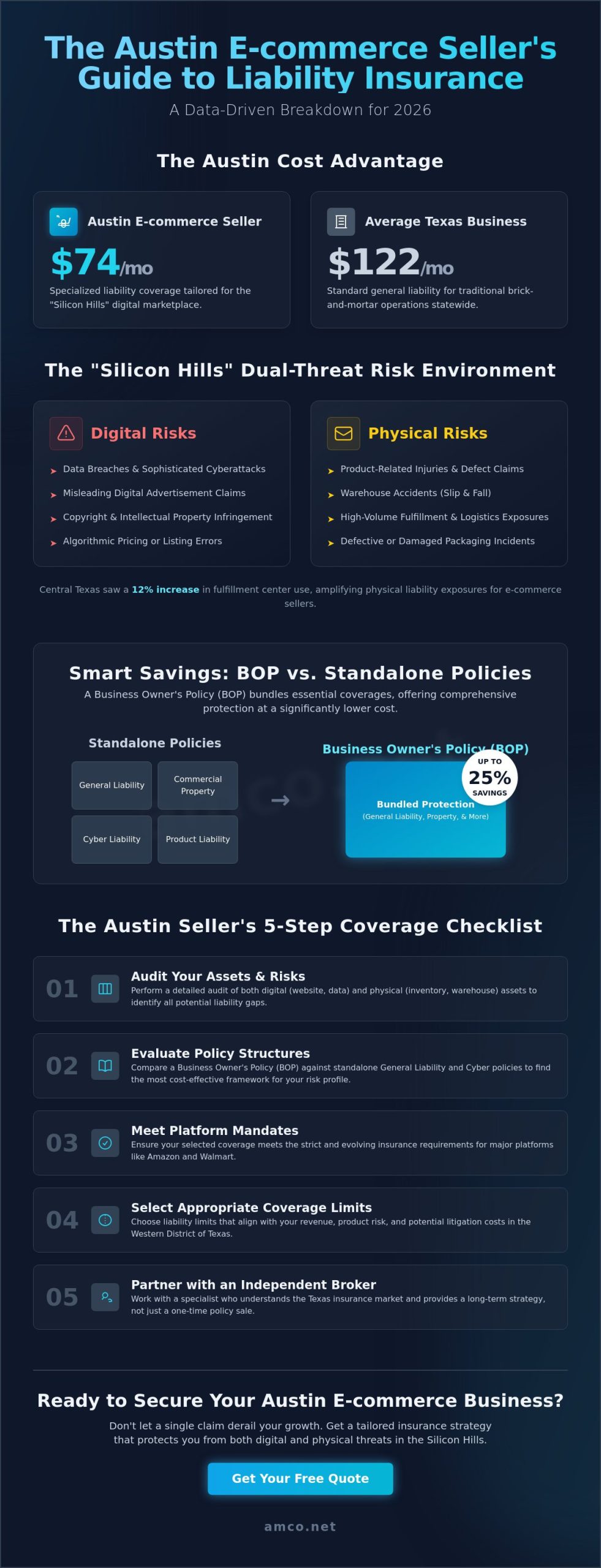

Did you know that while the average Texas business pays $122 monthly for general liability, an Austin-based e-commerce seller can often secure specialized coverage for approximately $74 per month? In the high-growth environment of the Silicon Hills, securing the right business liability insurance for e-commerce sellers in Austin is no longer just a checkbox for Amazon compliance; it's a fundamental component of your operational stability. You likely understand that a single product defect claim or a sophisticated cyberattack could jeopardize your entire enterprise. It's difficult to balance these digital risks with physical property needs while navigating Texas-specific insurance nuances.

This 2026 guide provides the technical precision required to evaluate your risk profile and select a policy that offers long-term value. We'll examine how bundling coverage into a Business Owner's Policy can reduce costs by up to 25%, detail the current 2026 premium trends in Central Texas, and outline the exact steps to protect your assets from both local and global retail liabilities. By focusing on data-driven risk management, you can ensure your business remains resilient against the evolving threats of the digital marketplace.

Austin's transition into the "Silicon Hills" has fundamentally altered the risk profile for digital entrepreneurs. Local sellers are no longer just shipping from a garage; they're integrated into a sophisticated tech-retail ecosystem that demands high-tier professionalization. Securing the right business liability insurance for e-commerce sellers in Austin is the technical foundation for this growth. While traditional retail focuses on physical premises, Austin's digital market presents a dual-threat environment. Sellers must manage physical risks, such as warehouse accidents or defective packaging, alongside digital threats like algorithmic errors or data breaches.

A standard Commercial General Liability (CGL) policy provides the baseline, but it often lacks the specific endorsements needed for 2026's digital-first liabilities. Generic policies fail because they don't account for the rapid scaling typical of Central Texas startups. You need a strategy that moves as fast as your revenue, ensuring that your protection evolves alongside your product line and order volume.

To better understand this concept, watch this helpful video:

Texas law, specifically under the Civil Practice and Remedies Code, places strict liabilities on sellers, even if they aren't the original manufacturer. Common lawsuit triggers in the digital space include product-related injuries and misleading digital advertisements. Austin businesses are also increasingly becoming targets for copyright infringement claims. The Western District of Texas has historically been a focal point for intellectual property litigation; this makes specialized business liability insurance for e-commerce sellers in Austin an essential defense. Without precise coverage, the cost of defending against a single "patent troll" could exhaust your company's cash reserves before the case even reaches discovery.

Securing business liability insurance for e-commerce sellers in Austin requires a granular understanding of how various policies interact to create a cohesive safety net. While the previous section highlighted the unique tech-retail ecosystem of the Silicon Hills, we must now examine the specific instruments that mitigate those risks. According to federal guidance on business insurance, most small enterprises require a combination of several coverages to remain fully compliant and protected.

General Liability (GL) serves as your foundational defense against third-party bodily injury and property damage. For an online store, its primary value often lies in advertising injury protection. This component covers claims of libel, slander, or copyright infringement within your digital marketing campaigns. Most Austin commercial leases for warehouse space or vendor contracts with local logistics providers mandate GL as a prerequisite. For broader regional insights, you can review our Comprehensive Guide to Insurance in Houston, TX: 2026 Industry Insights.

This is arguably the most vital coverage for anyone selling physical goods. Under the 'Stream of Commerce' rule, every entity in the distribution chain can be held liable for a defective product. Even if you aren't the manufacturer, you're legally responsible for the items you sell. Product liability covers not just the settlement, but also the legal defense fees, which frequently exceed the actual damage costs. Imagine an Austin-based startup selling a custom consumer electronic device. If a battery failure causes a fire in a customer's home, the resulting litigation could bankrupt an uninsured business before the first hearing concludes.

As e-commerce becomes more automated, the potential for data breaches increases. Cyber Liability is a non-negotiable shield for any business handling customer payment data. First-party coverage manages your immediate recovery costs and business interruption. Third-party coverage protects you if customers pursue legal action following a breach. In Texas, the Identity Theft Enforcement and Protection Act requires specific, time-sensitive notifications that carry significant financial penalties if neglected. Integrating a robust business liability insurance strategy allows you to focus on scaling your operations without the constant anxiety of digital theft or data loss.

Selecting the structural framework of your coverage is a technical decision that directly impacts your long term profitability. For many digital entrepreneurs, the choice lies between a Business Owner's Policy (BOP) and individual standalone contracts. Finding the right business liability insurance for e-commerce sellers in Austin often starts with this comparison. A BOP is designed for efficiency; it bundles General Liability and Commercial Property insurance into a single package. This streamlined approach isn't just about administrative ease. It typically offers a cost reduction of 15% to 25% compared to purchasing these policies separately, making it an ideal starting point for startups in the Silicon Hills.

However, you must be wary of the 'Scaling Trap.' As your business moves from a residential operation to a dedicated warehouse, your risk profile shifts. A standard BOP often has revenue caps or industry exclusions that might not accommodate high volume digital retail or high risk product categories. If your annual revenue surpasses the $5 million mark or you deal with complex electronics, you might require specialized product liability insurance with higher limits than a basic bundle provides. This ensures that your protection remains robust as your market share grows.

The primary benefit of a BOP is its comprehensive nature. Beyond basic liability, it includes Business Interruption coverage. This is vital in Central Texas, where unexpected events like the 2021 winter storm or localized power grid failures can halt operations for days. This coverage replaces lost net income and pays for ongoing expenses like payroll while your digital storefront is offline. To ensure your bundle is optimized for the local market, it's beneficial to consult an Insurance Company Near Me: Finding the Best Local Expertise in Texas for 2026.

Standard policies often require riders to cover the specific nuances of modern retail. Inland Marine insurance is a critical endorsement; it protects your inventory while it's in transit between your Austin facility and a global fulfillment center. If a courier vehicle carrying your stock is involved in an accident, standard property insurance won't cover the loss of goods on the road. Additionally, Hired and Non-Owned Auto coverage is essential if you or your employees use personal vehicles for business deliveries or supply runs. For those scaling their own logistics fleet, reviewing Commercial Trucking Insurance in Houston: The 2026 Essential Guide for Carriers can provide valuable perspective on managing transit risks across the Texas triangle.

Transitioning from a theoretical understanding of risk to the actual procurement of business liability insurance for e-commerce sellers in Austin requires a methodical approach. This is the stage where technical specifications meet operational reality. To ensure your 2026 growth remains unhindered by administrative or legal setbacks, follow this structured checklist to audit your current exposures and coverage requirements.

Insurers in 2026 prioritize data-driven risk management. To secure the most favorable rates, prepare a comprehensive documentation package that includes your 2026 revenue projections, detailed product specifications, and established safety protocols. Transparency regarding your manufacturing partners is a significant factor in cost optimization. A documented Quality Control (QC) plan demonstrates to underwriters that you have taken proactive steps to mitigate product failures, which can lead to a more precise and affordable premium structure.

The choice of a provider is as critical as the policy itself. While "online-only" insurers offer speed, they frequently use rigid underwriting models that might leave gaps in your local property coverage or fail to account for the nuances of Texas tort law. A local agent provides a consultative partnership, helping you decipher complex quotes where deductibles, aggregate limits, and specific exclusions are often buried in the fine print. This professional distance ensures you receive objective advice tailored to the Austin business climate. To begin your professional risk audit, you can get a technical assessment of your liability needs from a partner who understands the Texas market.

Choosing an insurance provider in the Silicon Hills often comes down to a choice between a generic algorithm and a strategic partner. Most direct carriers operate with a rigid, one-size-fits-all model that prioritizes their own bottom line. AMCO.NET LLC operates as an independent broker, which means we don't work for a single insurance company; we work exclusively for your Austin business. This independence allows us to audit the entire market to find the specific business liability insurance for e-commerce sellers in Austin that matches your unique risk profile. We provide the technical expertise necessary to ensure your digital and physical assets are protected without overpaying for unnecessary coverage.

Our firm has been a stable presence in the Texas insurance market since 1987. Over these four decades, we've guided businesses through massive regulatory shifts and economic cycles. This longevity isn't just a number; it's a testament to our reliability and deep understanding of Texas-specific liability climates. Whether you need a foundational General Liability policy or a complex commercial auto policy for your local delivery fleet, our advisors provide the professional distance and objective analysis required for high-level B2B decision-making. We move beyond the 1-800 number experience to offer a dedicated advisor who understands the Austin tech-retail ecosystem.

We leverage our long-standing relationships with top-tier national and regional carriers to secure competitive rates that aren't available to the general public. Our process involves an annual policy review, which is critical as your Austin e-commerce store scales from a home-based operation to a high-volume fulfillment center. AMCO.NET LLC is committed to providing fast, affordable, and expert-led insurance placement that prioritizes your operational continuity. By monitoring market trends and carrier performance, we ensure your coverage evolves alongside your revenue growth and technological advancements.

Working with AMCO.NET LLC is a methodical process designed for the busy entrepreneur. From the initial risk assessment to ongoing policy management, we handle the technical details so you can focus on product development and logistics. We understand that platform compliance is non-negotiable; therefore, we provide rapid access to your Certificates of Insurance (COIs) to satisfy Amazon, Walmart, or Etsy mandates within hours, not days. This efficiency reduces friction in your supply chain and protects your standing on global marketplaces. Secure your Austin business's future with a custom liability quote from AMCO.NET LLC and partner with a team that values your long-term stability.

Austin's digital economy requires a strategic risk management framework that scales with your ambition. We've examined how the transition to global fulfillment centers and the complexities of Texas product liability law necessitate specialized protection. By prioritizing a precise blend of general liability and cyber defense, you ensure your store remains resilient against both physical and digital disruptions. Securing the right business liability insurance for e-commerce sellers in Austin is a technical milestone that marks your transition into a professional, high-volume enterprise.

AMCO.NET has served Texas businesses since 1987, providing the local expertise needed to navigate the specific regulatory environments of the Austin and Houston markets. We leverage access to multiple A-rated insurance carriers to ensure your coverage is backed by financial stability and technical accuracy. Our advisors focus on long-term cost optimization rather than short-term fixes. Get a Fast & Affordable E-commerce Liability Quote from AMCO.NET and establish the security your business deserves. Your growth in the 2026 market depends on the stability of your foundation.

Texas law does not mandate general liability insurance for most private businesses, but contractual obligations usually make it essential. Landlords, lenders, and digital platforms like Amazon or Walmart require proof of coverage before you can operate. If your business owns vehicles, Texas law does require commercial auto insurance. While workers' compensation is optional for most private employers in the state, it remains a critical recommendation for risk mitigation.

The average cost for general liability insurance for e-commerce sellers is approximately $74 per month. If you opt for a Business Owner's Policy (BOP), which bundles property and liability, the average monthly cost is $106. Businesses operating in Austin's urban core may see premiums 10% to 15% higher than those in suburban areas. Factors such as your annual revenue and the specific type of products sold will influence your final rate.

Standard homeowners insurance policies typically exclude or severely limit coverage for business activities. Most personal policies won't protect your inventory if it's damaged by fire or theft; they also won't provide liability defense if a customer is injured by your product. To secure your assets, you need dedicated business liability insurance for e-commerce sellers in Austin that specifically addresses commercial risks and inventory storage.

General Liability provides a broad shield against third-party bodily injury, property damage, and advertising injuries occurring during your operations. Product Liability is a specialized subset that specifically covers damages or injuries caused by a defective product you sold. While General Liability covers a slip and fall at your office, Product Liability covers a battery explosion in a customer's home. Both are necessary for a comprehensive safety net.

You can obtain a Certificate of Insurance (COI) by contacting your insurance broker once your policy is active. Most major platforms have specific mandates; for instance, Amazon requires a $1 million liability limit once your monthly gross sales exceed $10,000 for three consecutive months. We provide these certificates quickly to ensure your digital storefront remains compliant and active without any administrative delays.

A data breach lawsuit triggers your Cyber Liability coverage to manage legal defense fees and potential settlements. In Texas, the Identity Theft Enforcement and Protection Act requires you to notify affected individuals within 60 days of discovering a breach. Your policy covers these notification costs, credit monitoring services for customers, and the technical forensic work required to identify the source of the security failure.

You can bundle your e-commerce coverage with commercial trucking or auto policies to achieve significant cost optimization. Bundling multiple lines of coverage with a single agency often results in premium discounts ranging from 15% to 25%. This approach also simplifies your administrative tasks by consolidating your renewals and certificates under one dedicated advisor who understands your entire logistics and retail operation.

Independent agencies provide access to multiple A-rated carriers rather than being limited to a single provider's products. We have served Texas businesses since 1987, offering a consultative approach that direct carriers cannot match. This allows us to compare the entire market to find the most efficient and affordable business liability insurance for e-commerce sellers in Austin based on your specific technical requirements and growth stage.