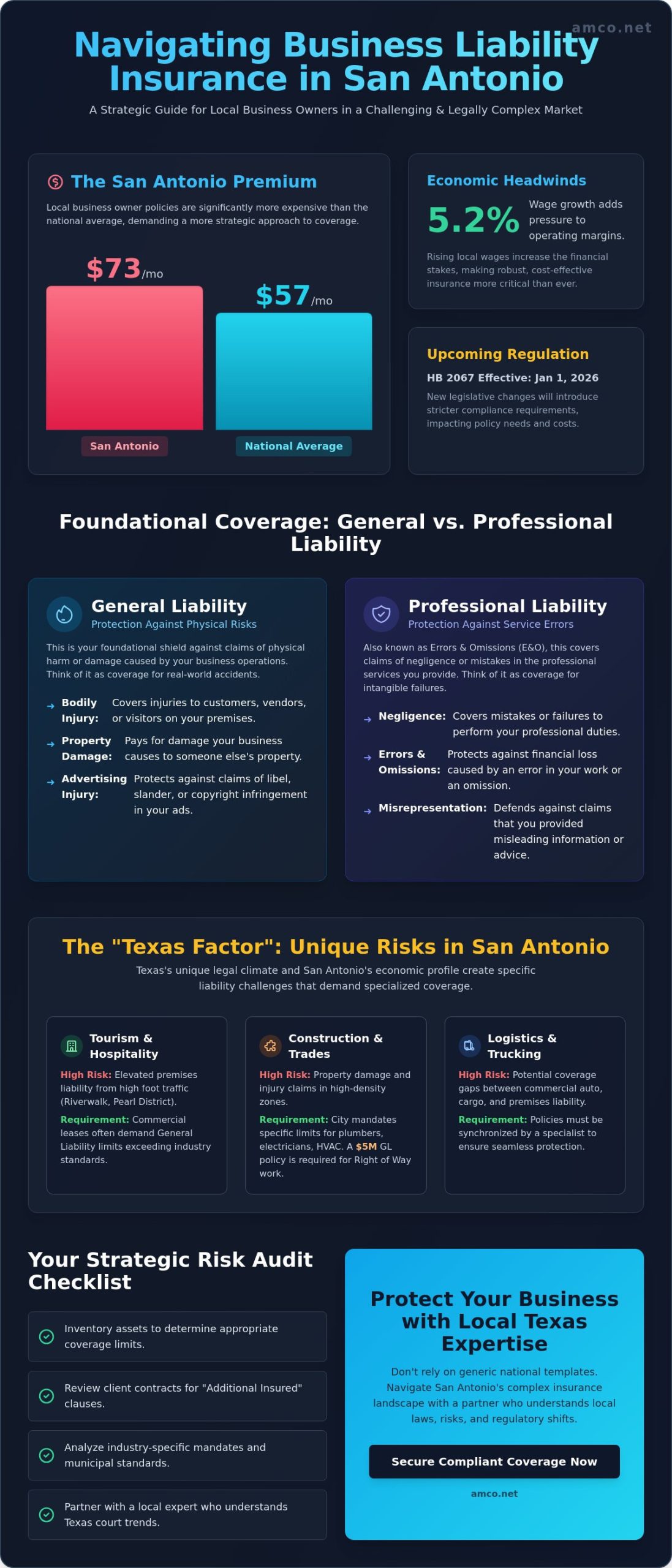

While San Antonio's economy saw a 5.2% wage growth through late 2025, local business owners now face a challenging insurance market where a standard Business Owner’s Policy costs $73 per month, which is significantly higher than the $57 national average. Securing the right business liability insurance San Antonio requires more than a basic policy; it demands a strategic alignment with the latest regulatory shifts, including the HB 2067 requirements effective January 1, 2026. You likely feel the pressure of rising premiums and the persistent fear that a single lawsuit could reveal a catastrophic gap between your General Liability and Professional Liability coverage.

We recognize that your priority is maintaining operational continuity without overpaying for redundant riders. This guide provides a technical framework to help you balance cost-effective premiums with the robust protection required by San Antonio commercial leases and industry-specific mandates. We'll examine the impact of 2026 legislative changes, clarify the critical distinctions between core liability types, and outline how to work with Texas-based experts to ensure your enterprise remains compliant and resilient in an increasingly litigious environment.

Business liability insurance San Antonio functions as a critical financial safety net, shielding your enterprise from the potentially devastating costs of third-party litigation. In the local market, where nominal hourly wages rose 5.2% in late 2025, the cost of a legal defense can quickly outpace your operating margins. Developing a deep understanding of commercial general liability is the first step in constructing a risk management framework that accounts for the "Texas Factor." This factor refers to our state's unique legal climate, characterized by complex liability statutes and a "non-subscriber" status for workers' compensation that places a higher burden of proof and financial responsibility on the business owner.

To better understand the core mechanics of this coverage, watch this helpful video:

The city’s heavy reliance on the tourism and hospitality sectors creates a high volume of foot traffic, particularly along the Riverwalk and the Pearl District, which elevates premises liability risks. Commercial leases in these high-demand areas frequently demand General Liability limits that exceed standard industry benchmarks to satisfy landlord indemnification clauses. San Antonio's position as a major logistics corridor means that general liability often overlaps with commercial trucking insurance, creating potential coverage gaps if your policies aren't synchronized by a specialist who understands the interplay between cargo and premises risks. San Antonio's rapid geographic expansion and infrastructure projects significantly increase the risk of property damage claims for local contractors working in high-density zones.

Texas law operates under a framework where business negligence is scrutinized through the lens of "Duty of Care." In a San Antonio courtroom, a jury evaluates whether your business took reasonable steps to prevent foreseeable harm to others. Local statutes, such as the Texas Civil Practice and Remedies Code, dictate how damages are awarded and how liability is apportioned among parties. Working with a Texas-based agent ensures your policy limits align with these specific legal standards, rather than relying on generic national templates that don't account for local court trends. This professional oversight is essential for maintaining the technological and financial continuity of your operations.

Understanding the distinction between physical risk and professional accountability is a prerequisite for any resilient risk management strategy. While many entrepreneurs view insurance as a singular protective layer, optimizing your business liability insurance San Antonio portfolio requires a more granular approach. General Liability serves as the foundation for physical risks, while Professional Liability addresses the intangible errors that can occur during service delivery. Deciding whether you need one or both depends entirely on your industry’s specific operational exposures.

A frequent challenge for San Antonio firms is identifying the "grey area" where these two coverages overlap. Imagine a scenario where a technician improperly installs a piece of heavy machinery. If the machine falls and injures a bystander, General Liability typically responds to the bodily injury claim. However, if the machine simply fails to operate, causing the client to lose $15,000 in daily production revenue, the claim shifts toward Professional Liability. For many small to mid-sized enterprises, a Business Owner’s Policy (BOP) offers an efficient solution. In Texas, a BOP averages $73 per month, effectively bundling General Liability with commercial property coverage to streamline premium costs.

General Liability (GL) is the primary defense against third-party claims of bodily injury or property damage. For retail shops in the Pearl or office spaces downtown, premises liability is the most common trigger. If a visitor sustains an injury on your property, GL covers the resulting medical expenses and legal defense fees. Manufacturers and distributors also rely on the product liability component of GL to protect against claims arising from defective goods. To see how these requirements compare across the state, you can review our Comprehensive Guide to Insurance in Houston, TX: 2026 Industry Insights for a broader perspective on Texas market trends.

As San Antonio’s technology and healthcare sectors expand, Professional Liability, also known as Errors and Omissions (E&O), has become indispensable. This coverage is designed for service-based businesses where a mistake, oversight, or failure to deliver a promised result leads to a client's financial loss without any physical damage occurring. While the median cost for E&O in Texas is $71 per month, San Antonio businesses often see an average of $91 per month due to the specific professional demographics of the region. Common triggers include data breaches, architectural errors, or professional negligence in consulting. If you are unsure which coverage applies to your specific service model, you can consult with an AMCO specialist to audit your current exposure levels.

San Antonio's economic structure demands a tailored approach to risk management that moves beyond generic policy templates. While the city's unemployment rate stood at 4.2% in November 2025, sector-specific volatility requires precise policy calibration to ensure long-term stability. Business liability insurance San Antonio isn't a one-size-fits-all commodity; a medical facility in the South Texas Medical Center faces vastly different exposures than a logistics firm operating near Port San Antonio. Identifying these nuances is the only way to avoid being underinsured during a high-stakes lawsuit.

The hospitality sector along the River Walk presents a high-density environment where premises liability risks are amplified by constant foot traffic and unique architectural constraints. For the city's burgeoning cybersecurity hub, the focus shifts toward cyber liability and data protection. As regulatory updates concerning data privacy expanded through early 2026, these coverages have transitioned from optional riders to essential components of a professional service contract. Balancing these industry-specific needs with affordable premiums requires a deep understanding of local market trends and court behaviors.

For San Antonio contractors, a standard General Liability policy is merely the entry point. To remain competitive and compliant, builders must secure "Completed Operations" coverage, which protects against claims arising after a project is finished and handed over to the owner. Many city-funded projects and large-scale commercial developments now mandate per-project limits to ensure that a claim on one site doesn't exhaust the coverage available for others. San Antonio's prevalent expansive clay soil often leads to foundation shifting and structural movement, creating a unique landscape for construction-related liability claims that standard policies might overlook. Furthermore, participants in the city’s Right of Way program must maintain $5 million in general liability coverage to meet municipal standards.

San Antonio serves as a vital inland port, making the interplay between General Liability and specialized transit policies critical for local carriers. While General Liability covers accidents on your premises or damage caused by your operations, it doesn't typically extend to cargo in transit. Integrating a Motor Truck Cargo policy ensures that your liability for the goods you carry is fully addressed. For a deeper analysis of fleet-wide risks, you can explore our Commercial Trucking Insurance in Houston: The 2026 Essential Guide for Carriers. Additionally, San Antonio auto repair shops and fleet maintenance hubs must prioritize garage-keepers liability to protect customer vehicles while they are in the business's care, custody, or control.

A methodical risk audit is the only way to ensure your business liability insurance San Antonio remains a functional asset rather than a sunk cost. As legislative changes like HB 2067 and SB 1455 took effect on January 1, 2026, the margin for error in policy documentation has narrowed. Conducting a five-step internal review allows you to identify vulnerabilities before they manifest as legal liabilities.

Performing these checks manually is time-consuming but necessary for financial continuity. To streamline this process and ensure you aren't missing local nuances, you can schedule a professional risk audit with an agent who understands the specific court trends in Bexar County.

The standard $1M/$2M policy is a common starting point, yet it often falls short for businesses in high-traffic zones or those handling high-value client assets. For these enterprises, Commercial Umbrella insurance provides an essential layer of protection that extends your primary limits. Factors driving premiums in San Antonio include your specific zip code; this is data the insurance department now publishes quarterly as of early 2026. Your historical claim frequency and the safety protocols you've implemented also play a heavy role in final underwriting decisions.

One of the most frequent errors is "Classification Error," where a business is listed under the wrong industry code. This lead to denied claims or expensive surprise audits. Many owners also overlook Hired and Non-Owned Auto (HNOA) exposure, incorrectly assuming their General Liability covers employees driving personal vehicles for business errands. Relying on a generic online policy often results in missing Texas-specific requirements, such as the $25,000 surety bond needed for insurance agencies or the $10,000 bond for notaries public. Precision in these details is what separates a stable operation from one vulnerable to regulatory fines.

Since 1987, AMCO has served as a cornerstone of the Texas business community, providing the technical expertise necessary to navigate a volatile insurance market. While automated platforms offer rapid quotes, they often lack the advocacy required when a San Antonio business faces a complex liability claim. Partnering with an independent broker gives you a strategic advantage; we maintain relationships with multiple top-tier carriers, allowing us to source the most competitive rates for business liability insurance San Antonio without compromising on the depth of your coverage. This model ensures you have a single, reliable point of contact for your General Liability, Commercial Trucking, and Surety Bond needs.

Local claims support is perhaps the most undervalued component of a policy until a lawsuit is filed. When your enterprise is served with a legal notice in Bexar County, you need an intermediary who understands local court trends and the specific nuances of Texas negligence statutes. Our team acts as your professional advocate, ensuring that the carrier meets its obligations and that your legal defense is robust. This personalized approach to risk management converts insurance from a mandatory expense into a stable foundation for your long-term growth.

Our established presence in both Houston and San Antonio provides us with unique regional insights that national call centers simply cannot replicate. We understand the specific pressures of the local economy, from the logistics demands of the I-10 corridor to the stringent insurance requirements of downtown commercial leases. By leveraging our decades of experience, we identify potential coverage gaps, such as the "Classification Errors" or "HNOA" exposures discussed in previous sections, before they become financial liabilities. If you are looking for an insurance company near me: finding the best local expertise in Texas for 2026 is the first step toward securing your firm's future. We pride ourselves on being the technical bridge between your business and the best-fit carriers in the industry.

True peace of mind comes from knowing your risk management framework is calibrated to the latest 2026 legislative standards and local market conditions. You don't have to navigate these complexities alone. Whether you're a contractor needing specialized per-project limits or a professional service firm seeking E&O protection, we provide the clarity and speed you require. You can easily access our resources through the AMCO mobile app or website to begin your assessment. Take the next step in securing your operational continuity today and get your fast and affordable business liability quote from AMCO.NET.

As the San Antonio market continues to evolve, maintaining a robust defense against liability becomes a strategic necessity rather than a clerical task. You've seen how legislative shifts like HB 2067 mandate greater transparency from insurers and how industry-specific risks in construction or logistics require precise policy limits. Effective risk management isn't just about paying premiums; it's about ensuring your business liability insurance San Antonio is calibrated to protect your specific operational continuity and long-term profitability.

AMCO has been serving the Texas business community since 1987, building a reputation for reliability and deep technical expertise. We leverage partnerships with A+ rated insurance carriers to provide the stability your enterprise deserves, while our mobile app allows for 24/7 policy management and instant access to certificates. This combination of traditional advocacy and modern convenience ensures your business remains resilient against unforeseen legal challenges. Your business represents years of dedication and hard work; let's work together to protect its future with precision and professional care.

Secure your San Antonio business today with a customized liability quote from AMCO.NET

Texas law doesn't mandate general liability for all businesses, but San Antonio municipal codes require it for specific trades. For example, plumbers, electricians, and HVAC technicians must maintain coverage to pull city permits. Contractors in the Right of Way program face even stricter requirements, needing $5 million in general liability. Contractual obligations in commercial leases often make it a functional requirement for most local enterprises.

Most small businesses in San Antonio pay between $40 and $90 per month for a standard $1M/$2M general liability policy. These rates are influenced by your specific industry and zip code data, which insurers must now report quarterly under HB 2067. Maintaining a clean claim history and implementing safety protocols can help keep your business liability insurance San Antonio premiums at the lower end of this scale.

General liability is a standalone policy focusing on third-party bodily injury and property damage. A Business Owner’s Policy (BOP) is a bundled solution that combines general liability with commercial property insurance. In Texas, the average BOP cost is $73 per month. This bundle is usually more cost-effective for small firms than purchasing separate policies for their physical assets and liability risks.

Consultants in San Antonio need professional liability insurance, also known as Errors and Omissions (E&O), because general liability only covers physical accidents. It won't protect you if a client sues over financial losses caused by your professional advice or a missed deadline. The average cost for this coverage in San Antonio is approximately $91 per month, providing a necessary shield for your professional expertise.

You can easily add an "Additional Insured" endorsement to your policy to satisfy commercial lease requirements. Landlords in high-traffic areas like the Pearl or Downtown San Antonio typically require this to ensure they're protected under your policy for claims arising from your business operations. It is a routine adjustment that our agents handle frequently to ensure your lease remains in good standing.

If a customer is injured at your location, your general liability policy’s premises liability coverage takes effect. It covers the customer’s medical bills and provides for your legal defense if the incident results in a lawsuit. Promptly documenting the incident and contacting your agent helps ensure the claims process moves efficiently, protecting your business from sudden out-of-pocket expenses related to the accident.

General liability does not cover injuries to your own employees. For work-related injuries or illnesses, you must carry Workers' Compensation Insurance. Although Texas is a "non-subscriber" state where coverage isn't strictly mandated for private employers, skipping this protection leaves your business vulnerable to personal injury lawsuits from employees. Relying on general liability for staff injuries is a common and dangerous misunderstanding of policy exclusions.

You can obtain a certificate of insurance (COI) almost instantly through the AMCO mobile app or our website. We understand that San Antonio contractors and service providers often need proof of coverage to access job sites or finalize contracts immediately. Our 24/7 digital policy management tools ensure that you don't have to wait for office hours to secure the documentation necessary for your operations.