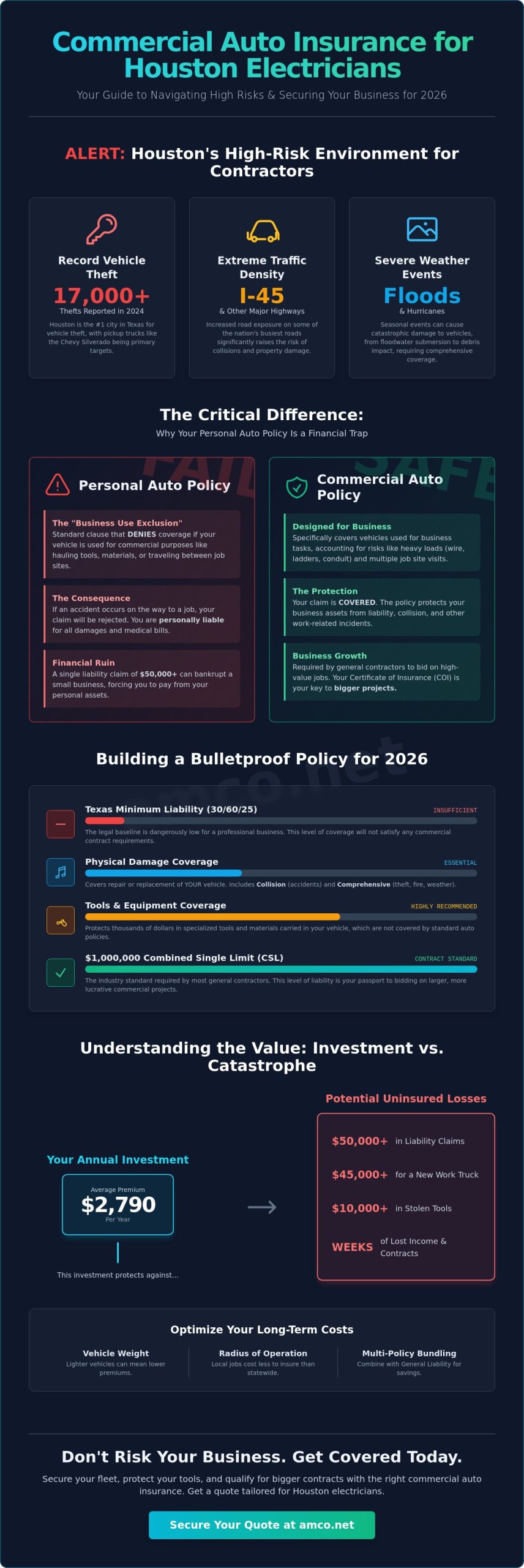

Houston reported over 17,000 vehicle thefts in 2024, the highest in Texas, with pickup trucks like the Chevrolet Silverado topping the list of targets. For a local contractor, losing a vehicle often means losing thousands of dollars in specialized equipment and weeks of billable hours. You likely already know that premiums are rising toward an average of $2,790 per year. Finding the right commercial auto insurance for electricians in Houston often feels like a constant battle between cost and coverage. It's frustrating to pay more while worrying if a personal policy will actually pay out during a job site incident.

This guide provides the technical clarity you need to secure a policy that protects your fleet, your tools, and your professional reputation. We'll examine the 2026 liability minimums, the necessity of the $1,000,000 Combined Single Limit for high-value commercial contracts, and specific strategies to mitigate Houston's unique high-theft risks. By focusing on long-term cost optimization and precise coverage, you can ensure your business stays compliant and operational on Texas roads.

Many electrical contractors in Harris County start their businesses using a personal truck, assuming their existing coverage is sufficient. This assumption often shatters when a claim is filed. The "Business Use Exclusion" is a standard clause in personal policies that explicitly removes coverage for any accident occurring while the vehicle is used for commercial purposes. Commercial auto insurance for electricians is a specialized policy that covers vehicles used for business tasks, including transporting tools, employees, and materials to job sites. Without it, you're essentially driving uninsured every time you head to a customer's location.

The risk profile for an electrician differs significantly from a standard commuter. Carrying heavy copper wire spools, industrial ladders, and conduit pipes changes the vehicle's center of gravity and braking efficiency. Texas law recognizes these increased risks, and insurance carriers price their products based on the higher probability of severe property damage. Relying on a personal policy isn't just a coverage gap; it's a structural flaw in your business model that can lead to total financial loss after a single collision on I-45. To protect your professional continuity, you need a policy designed for the weight and utility of a service van.

To better understand this concept, watch this helpful video:

Texas insurance regulations distinguish between "commuting" to a single place of work and "business operations" involving multiple job sites. If you're involved in an accident while transporting parts to a residential repair in The Heights, your personal carrier will likely deny the claim immediately. This denial leaves you personally liable for medical bills and vehicle repairs. For a small shop, a single $50,000 liability claim can lead to bankruptcy. Understanding the nuances of vehicle insurance is critical for maintaining operational continuity and avoiding such catastrophic outcomes. Professional coverage ensures that your assets remain protected even when your team is constantly on the move.

Beyond basic protection, having professional commercial auto insurance for electricians in Houston is a prerequisite for business growth. Most reputable general contractors in the Houston metro area now require subcontractors to carry a minimum of $1,000,000 in Combined Single Limit (CSL) liability. Your Certificate of Insurance (COI) serves as a professional passport, allowing you to bid on large-scale commercial builds or government contracts. Investing in the insurance houston experts recommend ensures you aren't disqualified from lucrative projects before you even submit a quote. It's about establishing yourself as a reliable, long-term partner in the local construction ecosystem while maintaining full compliance with site-specific safety and liability standards.

Structuring a robust policy requires more than just meeting the legal baseline. While Texas law mandates a minimum liability of 30/60/25 as of March 2026, these figures are insufficient for a professional enterprise. For those seeking commercial auto insurance for electricians in Houston, the focus must shift toward comprehensive protection that accounts for high-value assets and significant road exposure. Physical damage coverage is the first pillar, ensuring that if your specialized bucket truck or service van is damaged, the cost of repair or replacement doesn't halt your operations. This includes collision coverage for accidents and comprehensive coverage for non-collision events like fire or vandalism.

Beyond the vehicle itself, protecting the human element of your business is paramount. Motor vehicle safety protocols are vital, but insurance provides the financial safety net when accidents occur. In 2025, Harris County saw 2,758 serious injuries on its roadways. Uninsured and Underinsured Motorist coverage is essential in this environment, as it protects your team if a collision is caused by one of the many drivers in Houston operating without adequate protection. Similarly, Medical Payments or Personal Injury Protection (PIP) ensures that you and your apprentices receive immediate care regardless of fault, which is a standard expectation in a professional B2B environment.

Many electrical shops overlook the risk created when an employee uses their personal truck for a quick trip to Graybar or a supply house. If an accident occurs during this "parts run," your business can be held vicariously liable for damages. HNOA coverage is a cost-effective endorsement that extends your liability protection to these specific scenarios. It's a critical component for maintaining the technological and operational continuity that professional contractors expect, preventing a gap in coverage from turning into a corporate liability.

The $30,000 bodily injury limit required by the state is often exhausted by a single emergency room visit in today's economy. Most commercial projects now mandate a $1,000,000 Combined Single Limit (CSL) to even set foot on the job site. Balancing these high limits with your budget requires the guidance of a specialized insurance company near me that understands the Houston market's specific pressures. You can explore tailored options at amco.net to ensure your coverage aligns with both your risks and your growth objectives. This structured approach to liability prevents a single incident from compromising decades of hard-earned professional reputation.

Operating a fleet in the fourth largest city in the United States presents logistical challenges that directly influence your risk profile. The "I-45 Factor" refers to the extreme traffic density and high accident rates characteristic of Houston’s major arteries, including the 610 Loop and I-10. In 2025, Harris County recorded 2,758 serious injuries resulting from traffic accidents. For an electrical contractor, these statistics aren't just numbers; they represent a higher probability of collision claims. Insurance carriers analyze this local data to set premiums, meaning that commercial auto insurance for electricians in Houston must be structured to account for the frequent stop-and-go conditions and aggressive driving behaviors prevalent in the metro area.

Beyond the risks of the road, the physical environment of Southeast Texas introduces weather-related hazards. Flash flooding and hail damage are recurring events that can instantly sideline a service vehicle. Standard liability coverage does not provide protection against these environmental factors. To ensure business continuity, your policy must include comprehensive coverage. This technical layer of protection addresses non-collision damages, ensuring that a sudden storm or rising water levels in low-lying areas doesn't result in a total loss of your primary business assets.

While vehicle theft remains a significant concern, with over 17,000 incidents reported in Houston in 2024, electricians face a secondary "epidemic": tool theft. A standard commercial auto policy typically covers the vehicle itself but excludes the mobile inventory inside. If $5,000 worth of specialized testing equipment or power tools is stolen from your van while parked at a job site in high-risk areas like Greenspoint or Sharpstown, you may face a significant out-of-pocket expense. Inland Marine insurance, often called a "floater" policy, is the essential solution for this gap. It provides coverage for tools and equipment while in transit or stored at a temporary job site. Many contractors choose to bundle this with commercial trucking insurance Houston to achieve better cost-efficiency through multi-policy discounts.

The distinction between "Actual Cash Value" (ACV) and "Replacement Cost" is critical when selecting coverage for specialized work trucks. In the event of a total loss due to a hurricane or flood, an ACV policy only pays the depreciated value of the vehicle. For a modern, fully upfitted electrical van, this payout often falls short of the cost to purchase a new equivalent. Opting for replacement cost coverage ensures your business can return to full capacity without a capital shortfall. This level of foresight is a hallmark of professional risk management, providing the stability needed to navigate the volatile weather patterns of the Gulf Coast region.

Selecting the right commercial auto insurance for electricians in Houston involves a technical evaluation of your operational footprint rather than a simple price comparison. In 2026, insurance underwriters focus on three primary variables: your drivers' Motor Vehicle Records (MVRs), your radius of operation, and the Gross Vehicle Weight Rating (GVWR) of your fleet. If your business operates vehicles weighing 26,001 pounds or more, Texas law requires a minimum of $500,000 in Combined Single Limit (CSL) coverage. Even for lighter service vans, the professional standard remains $1,000,000 CSL. This higher limit is often the baseline requirement for achieving "Preferred Vendor" status with major Houston general contractors, who prioritize subcontractors with robust liability profiles.

Technology now plays a decisive role in premium optimization. Implementing telematics systems, including GPS tracking and dual-facing dashcams, provides the data transparency that carriers reward with lower rates. These tools don't just reduce premiums; they protect your reputation by providing objective evidence in the event of a "he-said, she-said" accident on congested routes like the Sam Houston Tollway. Bundling your auto policy with General Liability and Workers Compensation further stabilizes your costs through multi-policy discounts, creating a cohesive risk management framework for your enterprise.

A national call center often lacks the context to understand how a fleet breakdown near the Port of Houston impacts your billable hours. Working with a local agency ensures you have an advocate who understands the local market's fluctuations and provides hands-on claims support. Before signing, always verify the carrier’s A.M. Best rating. A rating of "A" or higher indicates the financial stability necessary to honor claims after large-scale events, such as the localized flooding common in Southeast Texas. This stability is essential for maintaining the technological continuity of your business operations.

Many contractors miss out on significant savings by failing to mention professional affiliations. Members of the Independent Electrical Contractors (IEC) or the National Electrical Contractors Association (NECA) often qualify for specialized group rates. Additionally, while not all your vehicles may require a Commercial Driver’s License (CDL), having CDL-certified drivers on your team signals a higher tier of professionalism to insurers. You can also reduce administrative costs by opting for annual paid-in-full plans rather than monthly installments. To find the most efficient structure for your specific fleet, you can request a professional quote from AMCO to compare current 2026 rates.

Use this checklist when reviewing your quotes:

Since 1987, AMCO has served as a strategic partner for the Texas business community, providing the stability and technical expertise required to manage complex industrial risks. For nearly 39 years, we've focused on delivering structured insurance solutions that go beyond simple policy issuance. When you seek commercial auto insurance for electricians in Houston, you aren't just looking for a standard contract; you're looking for a guarantee that your enterprise can survive the logistical and legal complexities of the local market. Our approach is consultative, treating every independent contractor with the same level of professional rigor we apply to major industrial accounts.

Efficiency is the cornerstone of modern electrical contracting. We understand that time spent managing insurance is time taken away from high-value service calls or critical infrastructure projects. That’s why we’ve optimized our platform to be mobile-friendly and responsive for the modern contractor. Whether you’re on a job site in Pearland or managing a crew in Sugar Land, you can handle your policy details without leaving the field. This commitment to technological continuity ensures your business remains agile, protected, and ready to meet the demands of any project owner.

Our agents possess a deep understanding of the specific equipment used in the electrical trade. We know that the risk profile of a residential service van differs fundamentally from that of an industrial bucket truck or a heavy-duty flatbed hauling transformers. We don't offer generic templates. Instead, we find the "sweet spot" where your premiums remain optimized but your protection levels meet the highest professional standards. By managing the administrative burden and technical paperwork, we allow you to focus on your core competency: keeping Houston’s power grid and commercial buildings operational. Our decades of experience mean we can anticipate the requirements of local general contractors before they even ask.

Securing your business shouldn't be a prolonged ordeal that slows down your operations. You can initiate a 5-minute online quote or speak directly with an expert who understands the nuances of the Houston metro area. Once your policy is active, the AMCO mobile app provides instant access to your Certificate of Insurance (COI). This feature is essential for contractors who need to provide proof of coverage to site managers on the fly to secure "Preferred Vendor" status. You can get a fast commercial auto quote for your Houston electrical business today and join the thousands of local professionals who have trusted our stability since 1987. We provide the comprehensive support you need to drive your business forward with confidence.

Securing your business against the volatile environment of Southeast Texas requires more than just meeting state minimums. A robust policy must bridge the gap between road liability and job-site equipment protection to ensure your operations remain uninterrupted. By prioritizing a $1,000,000 Combined Single Limit and specialized tool coverage, you position your firm as a preferred partner for Houston’s major general contractors in 2026.

Navigating the complexities of commercial auto insurance for electricians in Houston doesn't have to be a burden on your billable hours. Since 1987, AMCO has provided the technical expertise and stability needed to protect local fleets through A+ rated carriers. With our mobile-friendly platform, you can access an instant Certificate of Insurance (COI) directly from the job site; this ensures you never miss a contract opportunity due to a paperwork delay.

Request a Free Commercial Auto Quote for Your Houston Electrical Business today to optimize your costs and secure your professional legacy. We're ready to help you build a safer, more profitable future on Texas roads.

Texas law mandates minimum liability coverage for any vehicle operated on public roads. As of March 2026, the state minimum is 30/60/25 for bodily injury and property damage. While this meets the legal baseline, professional electricians usually need higher limits to comply with local licensing and general contractor requirements. Maintaining professional coverage is a structural necessity for any business operating in the Houston metro area.

Premiums vary based on fleet size and vehicle weight. As of October 2025, the average annual cost for an electrician was approximately $1,682. However, light-duty contractor vehicles in the Houston area often range between $250 and $320 per month as of March 2026. Factors like high local theft rates and I-45 traffic congestion contribute to these specific regional price points and risk assessments.

A standard commercial auto policy typically only covers the physical vehicle itself. It doesn't protect the specialized testing equipment or power tools stored inside. To protect your mobile inventory from theft or damage, you must add an Inland Marine endorsement, often called a tool floater, to your insurance package. This ensures your specialized gear is protected while in transit or at a job site.

The primary difference lies in the Business Use Exclusion found in personal policies. Personal insurance is designed for commuting and private use; it explicitly denies claims arising from commercial operations. Obtaining commercial auto insurance for electricians in Houston is necessary because it's specifically rated for the higher risks of transporting heavy materials and visiting multiple job sites daily across Harris County.

While some personal carriers offer small business riders, they rarely provide the high liability limits required for professional contracting. If you're hauling industrial spools or heavy ladders, a personal rider may still leave you underinsured in a serious accident. A dedicated commercial policy is the more reliable solution for maintaining professional continuity and meeting the safety standards expected by large scale project managers.

Most reputable Houston general contractors require a $1,000,000 Combined Single Limit (CSL). This industry standard ensures that a single accident doesn't exhaust your coverage limits. While state minimums are significantly lower, carrying the $1,000,000 CSL is often a prerequisite for bidding on commercial builds or government infrastructure projects. It serves as proof of your firm's financial stability and professional responsibility.

A history of violations or accidents significantly increases your risk profile and resulting premiums. Carriers in the Houston market scrutinize Motor Vehicle Records for the last three to five years. Frequent incidents can lead to high-risk surcharges or the exclusion of specific drivers from your policy. This directly impacts your operational capacity by limiting which team members can legally operate your service vehicles.

Bundling is a highly effective strategy for long term cost optimization. Most carriers offer a multi-policy discount when you combine commercial auto insurance for electricians in Houston with General Liability or Workers Compensation. This creates a cohesive risk management framework and simplifies your administrative work by consolidating your coverage under a single agency with a unified billing and claims support structure.