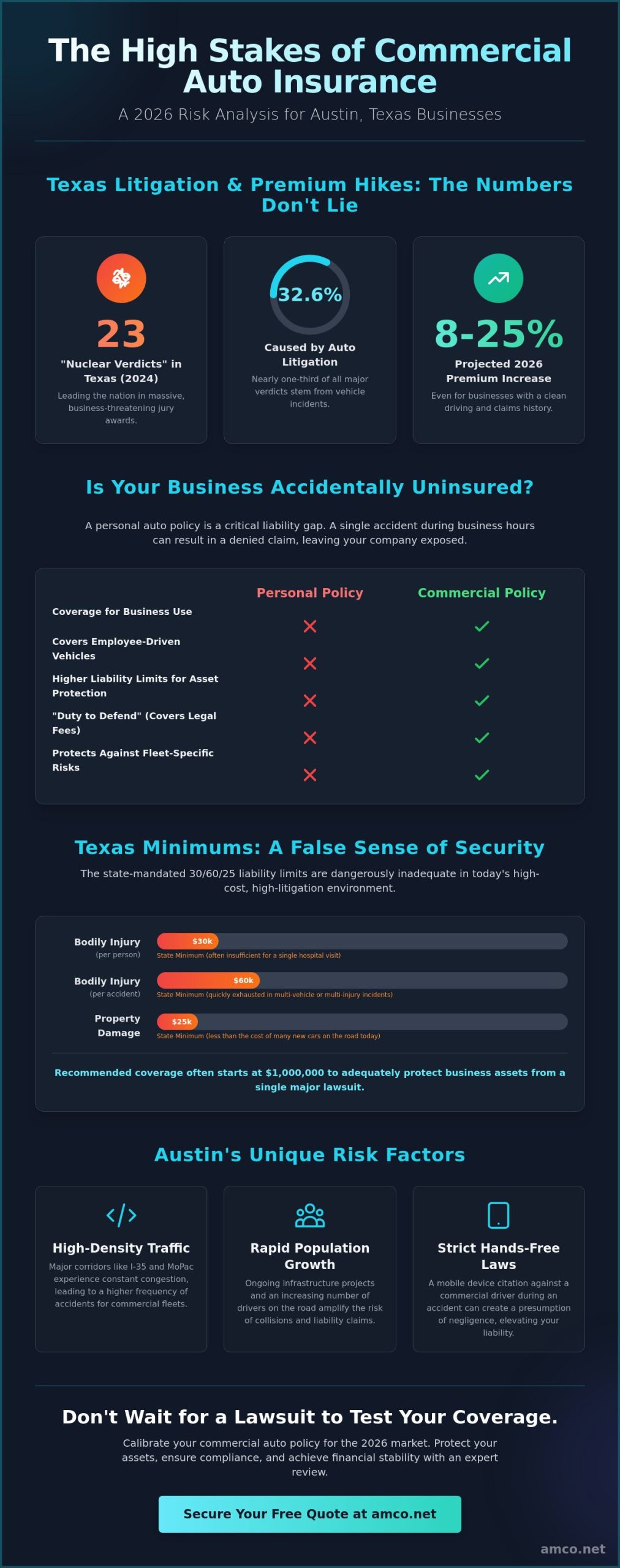

In 2024, Texas led the nation with 23 "nuclear verdicts," and 32.6% of those massive jury awards resulted from auto litigation. For business owners managing fleets in Central Texas, this data highlights a growing financial risk that goes far beyond simple fender benders on MoPac or I-35. Securing the right commercial auto insurance Austin policy is no longer just a checkbox for legal compliance; it's a critical component of your company's long term stability. You've likely seen your renewal premiums increase by 8% to 25% in 2026, even without a history of accidents or claims.

We understand that rising repair costs and new state regulations create a complex environment for your daily operations. This guide provides a detailed analysis of the current landscape, including the mandatory 30/60/25 liability limits and the implications of House Bill 2067, which took effect on January 1, 2026. You'll learn how to distinguish between personal and commercial policy boundaries to avoid costly coverage gaps. We also outline specific strategies to achieve predictable monthly costs while ensuring your business remains fully protected against the litigation trends currently impacting the Texas market.

Commercial auto insurance provides the technical framework to protect assets when vehicles are utilized for business operations. Whether your fleet consists of standard passenger cars or heavy-duty freight trucks, a specialized policy is required to manage the unique risks associated with commercial transit. Understanding What is Commercial Auto Insurance involves recognizing it as a contract that shields your company from the financial impact of collisions, property damage, and legal liabilities that standard personal policies specifically exclude.

For entrepreneurs in Central Texas, the necessity of commercial auto insurance Austin is driven by the city's rapid infrastructure expansion and the resulting traffic density. High-volume corridors like I-35 and MoPac have become synonymous with increased accident frequency. As Austin's population continues to grow, the complexity of managing a mobile workforce demands a policy that offers higher liability limits than those found in the consumer market.

To better understand this concept, watch this helpful video:

Many Austin business owners mistakenly assume their personal auto policy provides adequate protection. However, most personal insurers include a "business use" exclusion clause. If an employee is involved in an accident while delivering goods or traveling between job sites, the claim will likely be denied. This leaves the business owner personally responsible for all damages. For 2026, the Texas Department of Motor Vehicles (TxDMV) maintains minimum liability standards of 30/60/25; $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage. While these are the legal minimums, they rarely provide sufficient protection in a high-growth environment.

The population boom in the Austin metro area has led to a measurable increase in both accident frequency and the severity of claims. Local businesses often find themselves as primary targets for high-dollar litigation following even minor traffic incidents. Austin's strict hands-free ordinances mean that any commercial driver cited for mobile device use during an accident creates a presumption of negligence that significantly elevates the business's liability profile. Relying on commercial auto insurance Austin experts ensures your coverage aligns with these local legal realities.

A single collision on a major highway can lead to business bankruptcy if your liability limits don't account for modern medical costs and vehicle values. Commercial policies include a critical "Duty to Defend" provision, which requires the insurer to provide legal counsel and cover defense costs, regardless of the lawsuit's merit. This feature is vital for protecting your cash flow from unpredictable legal fees. If you're looking for a specialized Insurance Company Near Me, consulting with a local professional is the most effective way to calibrate your limits for the 2026 market.

Building on the legal foundations established by the state, a robust commercial auto insurance Austin policy requires a multi-layered approach to risk management. While the state-mandated 30/60/25 limits provide a baseline for operation, they rarely suffice for professional asset protection. Liability insurance remains the core component, covering bodily injury and property damage when your business is at fault. It functions as a financial buffer, preventing third-party medical bills or vehicle repairs from draining your company's capital reserves.

Physical damage coverage extends this protection to your own fleet assets. Collision coverage handles repairs following a traffic incident, while comprehensive coverage addresses non-collision events like theft, fire, or the high-intensity hail storms characteristic of Central Texas. For businesses managing a fleet, these coverages ensure operational continuity by facilitating rapid vehicle replacement. Adhering to Texas and federal insurance requirements is essential for maintaining compliance, especially for vehicles crossing state lines or carrying heavy loads.

Uninsured and Underinsured Motorist (UM/UIM) coverage is particularly vital in the Austin metro area. Despite legal mandates, a significant percentage of Texas drivers operate without active policies. UM/UIM fills the financial gap when a third party lacks sufficient coverage to pay for your damages. Additionally, Personal Injury Protection (PIP) or Medical Payments (MedPay) cover immediate medical expenses for your drivers and passengers. These ensure your team receives care regardless of fault, which is a key factor in maintaining workforce stability. Reviewing your specific risk profile with a specialist at amco.net can help identify which limits best suit your 2026 budget goals.

Employees often use their personal vehicles for business errands, creating a dangerous liability gap. Hired and Non-Owned Auto (HNOA) insurance protects your business if an employee causes an accident while driving for work purposes. Austin’s tech startups and service providers frequently overlook this risk, assuming personal policies will cover the damage. However, as discussed previously, business use exclusions often leave the company exposed to litigation that HNOA is specifically designed to mitigate. It integrates seamlessly with your existing liability framework to provide 24/7 protection.

For contractors and distributors, the vehicle's value is often secondary to the cargo it carries. Specialized cargo and inland marine insurance protect goods in transit from loss or damage. This is a distinct risk from vehicle damage; a truck might survive a minor collision while its temperature-sensitive or fragile contents are destroyed. For carriers operating between major Texas hubs, understanding Commercial Trucking Insurance in Houston is equally important, as it details the specific endorsements required for high-capacity transport in the Gulf Coast region.

Understanding the variables that determine your premium is essential for long term cost optimization. In 2026, insurance carriers utilize granular data and predictive modeling to assess risk profiles with engineering-like precision. Your premium isn't a static number; it's a reflection of several operational factors that you can influence through proactive management. When evaluating commercial auto insurance Austin, the primary garage location serves as the baseline for these calculations.

The "Austin Zip Code" factor plays a significant role in rate determination. A business operating out of Downtown Austin (78701) faces higher traffic density and a statistically greater risk of theft or vandalism compared to a facility located in Round Rock or Pflugerville. Beyond geography, the vehicle type and its intended usage are critical. A heavy-duty freight truck requires significantly higher premiums than a standard plumber’s van because the potential for catastrophic damage in a collision is much greater. Carriers also scrutinize Motor Vehicle Reports (MVRs) for every driver on your team. A single speeding ticket or minor citation can trigger a premium surge, as driving history remains the most reliable predictor of future claims.

Your claims history, specifically a documented three-year loss run, serves as your strongest negotiation tool. Carriers prefer businesses that demonstrate a consistent pattern of safety and few, if any, paid claims. This historical data provides the leverage needed when learning how to choose the best policy that balances comprehensive protection with fiscal responsibility.

The distance your vehicles travel impacts your risk exposure. Driving exclusively within Austin city limits involves frequent stops and urban parking, which increases the likelihood of minor comprehensive claims. Conversely, long-haul routes across the state introduce risks related to driver fatigue and high-speed highway transit. As of May 2026, inflation has driven vehicle replacement values up by 12% across Texas, leading to a proportional rise in comprehensive premiums regardless of your operational radius.

Implementing a formal driver safety program offers a measurable return on investment. Documented training sessions and strict maintenance schedules don't just lower your risk of accidents; they also protect your business from "negligent maintenance" claims during litigation. For companies managing a multi-city fleet, comparing your local rates with Car Insurance in Houston, TX can provide a broader perspective on how regional safety data influences Texas insurance markets.

Strategic cost-management is the cornerstone of sustainable fleet operations. In a market where premiums fluctuate based on regional data, business owners must adopt a systematic approach to policy selection. One of the most effective methods for immediate reduction is bundling. By integrating your commercial auto insurance Austin policy with General Liability or a comprehensive Business Owners Policy (BOP), carriers often apply multi-policy discounts. These credits reflect the reduced administrative overhead for the insurer and can lead to measurable savings on your annual statement.

Adjusting your deductible serves as another lever for cost-optimization. Increasing a deductible from $500 to $1,000 can significantly lower monthly premiums, provided the business maintains sufficient liquidity to cover the higher out-of-pocket expense during a loss. This decision should be based on a thorough analysis of your claims frequency. Performing an annual policy audit ensures your coverage limits align with your current fleet size and revenue. As your Austin business scales, an outdated policy may leave you exposed or cause you to pay for redundant protection that no longer serves your operational goals.

The adoption of telematics has transformed from a niche technology to an industry standard for 2026. Usage-Based Insurance (UBI) utilizes real-time data from GPS and driving monitors to provide carriers with objective proof of safe behavior. Instead of relying on general regional statistics, your premiums are calculated based on actual performance metrics, such as braking patterns and speed adherence. This transparency allows high-performing fleets to secure rates that are often 15% to 20% lower than traditional actuarial estimates. Modern encrypted systems ensure data security while maximizing fleet efficiency and driver accountability.

The Texas insurance market remains volatile, requiring a partner who can scan the entire landscape rather than a single provider. Unlike "captive" agents who represent only one company, independent brokers like AMCO.NET LLC have access to multiple top-tier carriers. This competitive environment forces insurers to bid for your business, ensuring you receive the most favorable terms available. For those managing operations across the state, reviewing our Comprehensive Guide to Insurance in Houston provides the necessary context for multi-city risk management. To begin optimizing your fleet's financial performance, request a professional policy review from AMCO.NET LLC today.

Since 1987, AMCO.NET LLC has operated with a commitment to technical precision and professional reliability. In the B2B sector, insurance isn't merely a commodity; it's a critical industrial solution that ensures business continuity. We approach commercial auto insurance Austin with the same analytical mindset a manufacturer uses to optimize a complex production line. This longevity in the Texas market provides our clients with a sense of stability that newer agencies cannot replicate. We understand that fleet management requires long term continuity and a deep understanding of the local regulatory environment, especially as Texas laws evolve in 2026.

Our expertise extends across the entire state of Texas, allowing us to support Austin-based businesses as they expand into Houston, Dallas, or San Antonio. While we utilize modern digital tools and a dedicated mobile app for policy management, we maintain a firm belief in the necessity of expert human intervention. You won't be routed through an anonymous call center when you have a technical question about your coverage. Instead, you'll have direct access to experienced agents at AMCO.NET LLC who understand the specific challenges of operating a commercial fleet on high-traffic urban corridors.

We don't just sell policies; we partner with you to optimize your business safety profile. By analyzing your claims history and operational radius, AMCO.NET LLC identifies areas where risk can be mitigated before an accident occurs. This proactive stance is essential for maintaining predictable insurance costs in a volatile market where premiums are rising. Our team provides fast, accurate quotes tailored to the unique technical requirements of your industry, whether you operate light service vans or heavy-duty industrial transport vehicles. We prioritize transparency and long-term client stability over short-term sales targets.

To ensure the most efficient and accurate quoting process, we recommend preparing a comprehensive driver list and a complete set of vehicle Identification Numbers (VINs) before your initial consultation. During your first meeting with an AMCO.NET LLC commercial specialist, we'll conduct a thorough review of your current coverage to identify potential gaps or redundancies that could lead to financial loss. This methodical approach ensures that your final policy is both cost-effective and technically sound for the 2026 market. Secure your Austin business today with an AMCO.NET LLC commercial auto quote.

Partnering with a specialist who understands the nuances of commercial auto insurance Austin is the most efficient way to ensure your fleet remains compliant and cost-effective. Since 1987, AMCO.NET LLC has provided Texas businesses with the consultative expertise needed to manage complex B2B risks with engineering-like precision. We provide access to top-rated commercial carriers, ensuring your policy is calibrated for both maximum protection and long term ROI.

Get a Fast & Professional Commercial Auto Quote for Your Austin Business and take the first step toward a more secure, predictable financial future. We look forward to helping your business thrive on the roads of Central Texas.

Yes, you need specialized coverage because most personal auto policies contain a "business use" exclusion that denies claims occurring during work tasks. Even occasional deliveries or client visits can trigger a denial if an accident happens while the vehicle is being used for a commercial purpose. Securing a commercial auto insurance Austin policy ensures your business assets remain protected during these professional trips, regardless of their frequency.

The average cost for commercial auto insurance in Texas typically ranges from $150 to $1,072 per month, depending heavily on your industry and vehicle type. For instance, a standard sedan may cost around $150 monthly, while transportation and logistics companies often pay closer to $458 per month. These rates reflect the 12% inflation-driven increase in vehicle replacement values and repair costs observed across the state as of May 2026.

Standard policies do not automatically cover employees' personal vehicles; you must add Hired and Non-Owned Auto (HNOA) coverage to protect the business. This endorsement provides liability protection for your company when staff members use their own cars for work-related errands or deliveries. Without HNOA, your business could be held responsible for damages that exceed the employee's personal policy limits following a collision on Austin's crowded infrastructure.

The State of Texas mandates a minimum liability coverage of 30/60/25 for all commercial vehicles in 2026. This requires $30,000 for bodily injury per person, $60,000 for bodily injury per accident, and $25,000 for property damage per accident. While these TxDMV standards meet legal requirements, many Austin businesses opt for higher limits to shield themselves from the rising frequency of high-value litigation and "nuclear verdicts" in the region.

You can integrate your commercial auto insurance Austin policy with General Liability or a Business Owners Policy (BOP) to access multi-policy discounts. Carriers often reduce premiums when you consolidate coverages because it lowers their administrative overhead. This strategy not only provides a more predictable monthly cost but also ensures your risk management framework is cohesive, leaving no gaps between your automotive and general business liability protections.

Your personal driving history and the records of every employee on your team directly impact your commercial premiums. Insurance carriers use Motor Vehicle Reports (MVRs) to assess risk; a single speeding ticket or at-fault accident can lead to a rate increase of 8% to 25% during your next renewal. Maintaining clean records across your entire workforce is the most effective way to prove safe behavior and secure lower actuarial rates.

Accidents involving unlisted drivers frequently result in denied claims or significant legal complications for the business owner. Commercial insurers require all regular operators to be disclosed and vetted before they get behind the wheel. If an undisclosed driver causes an accident, the carrier may refuse to provide a "Duty to Defend," leaving your company to pay for all legal fees and third-party damages out of pocket.

Standard commercial auto insurance covers the physical vehicle but does not protect the tools, equipment, or cargo stored inside. To protect these assets, you need an Inland Marine or specialized cargo endorsement. This coverage ensures that if your professional equipment is stolen from a job site or damaged during transit, the financial loss is covered, as the base auto policy only addresses the vehicle's structural damage.