Would your operations remain stable if a single hailstorm triggered a deductible costing thousands of dollars more than you anticipated? Most carriers for commercial property insurance Dallas have transitioned to a 2% wind and hail deductible instead of a fixed dollar amount. This shift means your financial responsibility increases automatically as your property value climbs. It's a specialized challenge that requires a precise, technical understanding of your policy's fine print.

We recognize the frustration of managing rising premiums while trying to decipher complex jargon like "coinsurance" or "named perils." You've likely seen your property valuations soar, and you need a strategy that protects those assets without compromising your company's liquidity. This guide provides a professional roadmap to the 2026 DFW market, helping you identify essential coverages and avoid costly gaps in business interruption protection. We'll examine the latest Texas Department of Insurance data, the critical role of Ordinance and Law coverage, and how to structure a policy that withstands the unique volatility of the North Texas climate.

Commercial property insurance Dallas serves as a critical safeguard for the physical foundations of your enterprise. This coverage protects your fixed assets from perils such as fire, vandalism, and the specific environmental hazards prevalent in North Texas. Dallas businesses navigate a risk landscape that differs significantly from coastal or rural regions. Rapidly rising property values in the DFW Metroplex mean that underinsurance is a constant threat. While an insurance in Houston strategy might focus on flood zones and hurricane surges, a Dallas plan must account for the high frequency of severe hail and wind events that define our local climate.

A comprehensive policy differentiates between real property and business personal property (BPP). Real property includes the physical building and any permanent additions, such as HVAC systems or built-in cabinetry. BPP covers the portable assets inside those walls. For many organizations, these elements are integrated into a Business Owner's Policy (BOP) to ensure a cohesive risk management approach. This integration is vital for maintaining operational continuity in a market where replacement costs for materials and labor are rising steadily.

A standard policy in Dallas protects a broad range of assets, including office furniture, specialized manufacturing equipment, computers, and exterior signage. Most modern policies are written on an "Open Perils" basis. This means the policy covers all causes of loss unless they are specifically excluded. In contrast, a "Named Perils" policy only covers events explicitly listed in the document. For tenants who lease their space, BPP coverage is the most vital component. It ensures that your investment in inventory and improvements remains protected even if you don't own the building's shell.

Property damage is only the first phase of a loss. Business Interruption coverage, often called Business Income insurance, replaces lost revenue when your operations cease due to a covered event. Imagine a severe spring hailstorm that shatters skylights and causes significant water damage to your server room. If your facility is unusable for three weeks, this coverage helps pay for ongoing expenses like payroll and taxes. Additionally, "Extra Expense" coverage provides the liquidity needed to relocate to a temporary site quickly, ensuring that a physical disaster doesn't lead to a permanent loss of your customer base.

Securing comprehensive commercial property insurance Dallas requires a granular look at the specific assets that drive your revenue. While the building structure is the most visible component, a professional policy must account for permanent fixtures, machinery, and outdoor property. For instance, integrated HVAC systems or custom-built manufacturing lines are often classified under building coverage rather than contents. This distinction is vital for accurate valuation and claim processing. As noted by Forbes Advisor on commercial property insurance, understanding these nuances prevents significant out-of-pocket expenses during a total loss event.

Technology-dependent businesses in North Texas face unique risks that standard policies often overlook. Electronic Data Processing (EDP) coverage is a specialized endorsement that protects servers, laptops, and data storage devices from perils like power surges or hardware failure. Similarly, if your operations involve transporting expensive tools or specialized equipment between job sites, Inland Marine insurance is necessary. This coverage follows the equipment wherever it goes, filling the gap left by static property policies. For property owners who lease space to others, Lessor’s Risk Only (LRO) provides the specific liability and property protections needed for commercial landlords. If you're unsure which endorsements fit your operational model, reviewing your current commercial property insurance Dallas options with a specialist can clarify these technical requirements.

Accurately valuing inventory for 2026 market rates is a complex task. Dallas businesses must account for local supply chain fluctuations that affect equipment replacement timing and cost. If you've invested in renovations for a leased space, "Improvements and Betterments" coverage is essential. This ensures that the high-end finishes or specialized wiring you installed are protected, even though you don't own the building shell. Keeping an updated asset ledger helps maintain policy accuracy as your business scales.

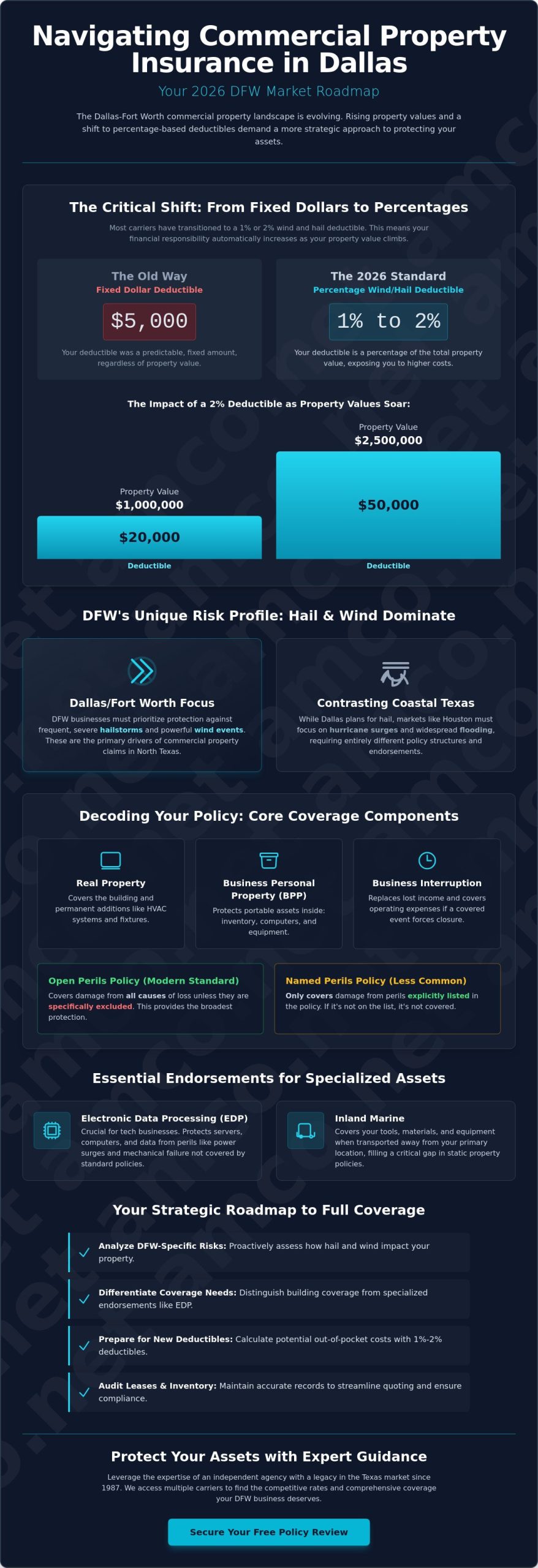

North Texas weather isn't just a topic for local news; it's the primary driver of commercial property insurance Dallas rates and policy structures. The DFW Metroplex experiences a high frequency of severe convective storms that bring damaging hail and straight-line winds. These events have forced a fundamental shift in how carriers manage risk. In 2026, the transition from flat-dollar deductibles to percentage-based deductibles is nearly universal for inland Texas properties. This change significantly alters the financial responsibility of the policyholder during a claim.

A 2% wind and hail deductible is now the standard baseline for most commercial assets in Dallas. For a facility insured at $1,000,000, the business owner is responsible for the first $20,000 of storm damage before the carrier contributes. This structure requires businesses to maintain higher liquidity to cover potential repairs after a spring storm. Beyond deductibles, the "Coinsurance Trap" remains a severe threat to operational stability. If a property is undervalued on the policy, the insurer can apply a proportional penalty to the payout. This means that if you insure your building for only 70% of its true value, the carrier may only pay 70% of a partial loss, leaving your business to fund the remaining gap.

Percentage-based deductibles create a variable cost that grows as your property value increases. To manage this risk, businesses should prioritize roof maintenance and material upgrades. Installing impact-resistant roofing materials can sometimes negotiate better terms or lower the percentage required by the carrier. It's also vital to have a dedicated contingency fund. Relying on a flat-dollar expectation is a tactical error in the current North Texas market; you must calculate your exposure based on the total insured value of your assets.

The Dallas construction market has seen significant inflation in both labor and material costs. Using 2022 or 2023 property valuations for a 2026 policy is a dangerous strategy that almost guarantees a coinsurance penalty. The "limit of insurance" must reflect what it would cost to rebuild today, not what the building cost five years ago. A professional appraisal is the most effective defense against these penalties. It provides a documented, data-driven valuation that ensures your coverage limits align with current market realities, protecting your company's long-term financial health.

Choosing between Actual Cash Value (ACV) and Replacement Cost Value (RCV) is another critical decision. RCV is generally the preferred choice for businesses that intend to remain operational after a loss. While ACV might offer lower premiums, it deducts for depreciation. In a high-inflation environment, the difference between an ACV payout and the actual cost of new equipment or construction can be catastrophic for a company's cash flow.

Securing a robust policy requires a methodical approach that extends beyond a simple price comparison. Before requesting a quote for commercial property insurance Dallas, you must compile a technical profile of your assets. This documentation should include the building's construction classification, the precise age of the roofing system, and a detailed inventory of security and fire suppression technologies. Providing this data upfront allows carriers to assess your risk profile with greater precision, which often leads to more favorable terms. If your operations also involve a fleet of vehicles, it's efficient to align these efforts with your other regional coverage needs by reviewing our guide on local auto insurance.

A critical step in this evaluation is the audit of your current lease agreement. Many business owners overlook the specific insurance mandates embedded in their contracts. Working with an independent agency allows you to compare multiple carriers simultaneously. This is particularly advantageous in the 2026 market, where carrier appetites for Dallas-based risks fluctuate. By accessing a broader range of underwriters, you can find specialized solutions that a single direct writer cannot provide. To ensure your coverage limits align with your actual contractual obligations, you can start your policy evaluation with AMCO today.

In the Dallas commercial real estate market, Triple-Net (NNN) leases are the standard for retail and industrial spaces. Under these terms, the tenant is typically responsible for the property's taxes, maintenance, and insurance costs. A common point of contention in North Texas involves the HVAC system. Many leases mandate that the tenant maintains and insures the rooftop units, which are highly susceptible to hail damage. Even if the landlord insures the building shell, tenants must maintain their own property and liability coverage to protect their specific operational interests and improvements.

When reviewing potential policies, you must ask specific questions about exclusions and timeframes. Standard property policies in Dallas usually exclude flood and earthquake damage. If your facility is near a flood plain or involves high-vibration industrial processes, you may need separate endorsements. Additionally, clarify how the policy treats external assets like signage, fencing, and landscaping. Finally, ask about the "period of restoration" for business income coverage. This timeframe determines how long the carrier will pay for lost revenue while your Dallas facility is being repaired or rebuilt.

AMCO has served the Texas business community since 1987. This extensive history provides us with a unique perspective on the cyclical nature of the DFW market. Unlike captive agents who represent a single carrier, our independent status enables us to shop multiple underwriters on your behalf. This is essential for securing commercial property insurance Dallas because it ensures you aren't limited by one company's changing risk appetite for North Texas weather events. We analyze the market to find the intersection of comprehensive coverage and fiscal responsibility, ensuring your premiums align with the actual risk profile of your assets.

Professional risk management requires more than an automated algorithm. Our advisors conduct thorough assessments to identify vulnerabilities that digital platforms often miss. We examine your entire operational footprint to provide a cohesive solution. For businesses with logistical components, we seamlessly integrate property protection with commercial trucking insurance in Houston and Dallas. This holistic approach prevents coverage silos and ensures that every asset, from your warehouse to your fleet, is protected under a unified strategy that emphasizes technological continuity and financial stability.

Our team possesses a deep technical understanding of Texas regulations and the specific perils that threaten DFW businesses. We know that in a B2B environment, time is a critical resource. That's why we prioritize fast, responsive support for certificates of insurance (COIs) and claim processing. Our consulting is transparent and data-driven. We provide clear explanations of policy terms, helping you make informed decisions without the distraction of aggressive marketing tactics. We focus on your security and the long-term viability of your operations.

Protecting your company's future in the DFW area starts with a precise evaluation of your current exposure. Our philosophy centers on providing fast and affordable solutions that don't sacrifice technical depth. We invite you to contact our team for a customized risk review that addresses the complexities of the 2026 market. Whether you're a growing firm or an established enterprise, we offer the stability and professional expertise required to navigate the evolving Texas insurance landscape. Let's build a resilient foundation for your operations together. Reach out today to secure your commercial property insurance Dallas with a partner who understands your local challenges.

Protecting your enterprise in the North Texas market requires a strategic alignment with local environmental realities. You've seen how the shift toward 2% wind and hail deductibles and rising construction costs have redefined the 2026 landscape. Maintaining accurate property valuations is essential to avoid the coinsurance trap during a claim. By prioritizing specialized endorsements like Ordinance or Law and Business Interruption, you ensure that your business remains resilient against the volatility of the spring storm season.

AMCO has been serving Texas businesses since 1987. As an independent agency, we represent top-rated carriers to provide the specific expertise needed for high-risk North Texas weather coverage. We deliver complex system solutions tailored to your unique operational footprint rather than generic products. To secure a policy that balances technical depth with fiscal efficiency, Get a Fast & Affordable Dallas Commercial Property Quote from AMCO. Our team is ready to help you navigate the complexities of commercial property insurance Dallas so you can focus on your company's growth. Your stability is our priority as we work together to protect your business's future.

It typically covers the physical structure of your building and the tangible assets housed within it. This includes specialized machinery, office furniture, and exterior signage against perils like fire or vandalism. In the North Texas region, it also provides the primary layer of protection against severe windstorms and hail damage. This ensures that your operational foundation remains secure even after significant environmental disruptions or physical property crimes.

No, standard policies almost universally exclude damage caused by rising surface water or overflowing bodies of water. Dallas business owners must secure a separate flood insurance policy or a specific endorsement to protect their assets from this risk. It's a critical distinction for properties located near the Trinity River or in low-lying urban drainage areas where flash flooding can occur during heavy spring rains.

The cost of commercial property insurance Dallas varies based on factors such as building age, construction materials, and the specific industry risk profile. Proximity to fire hydrants and the installation of modern fire suppression systems also influence the final rate. Choosing higher deductibles for wind and hail can mitigate premium costs, though it increases your out-of-pocket responsibility during a claim. Each policy is tailored to the specific asset's replacement cost.

A coinsurance clause requires you to maintain a coverage limit equal to a specific percentage of your property's actual value, often 80% or 90%. If your Dallas business is underinsured when a loss occurs, the carrier applies a penalty that reduces your claim payout proportionally. This makes regular appraisals vital in the rapidly appreciating commercial property insurance Dallas market to ensure your limits accurately reflect current reconstruction costs and labor rates.

Yes, because standard homeowners policies typically provide very limited coverage for business-related equipment and inventory. If you store significant stock or expensive professional gear in a Dallas home office, you likely need a home-based business endorsement or a standalone policy. This ensures your professional assets are protected from fire, theft, or damage that your personal insurance might exclude while you are conducting business operations from your residence.

In North Texas, these deductibles are usually calculated as a percentage of the total insured value of the building rather than a flat dollar amount. For example, a 2% deductible on a $500,000 property means the business owner pays the first $10,000 of a claim. This structure is the industry standard for managing the high frequency of hail events in the Dallas area and requires businesses to maintain liquid contingency funds.

You can frequently bundle property coverage with general liability insurance into a Business Owner's Policy. This approach often provides a more cost-effective solution than purchasing standalone policies while simplifying your administrative management. It's a common strategy for small to mid-sized Dallas firms looking to secure comprehensive protection for both their physical assets and their legal liabilities under a single, cohesive insurance program that streamlines the renewal process.

Business Personal Property covers the movable assets your company owns, such as inventory, computers, and office furniture. It's essential for tenants who lease their space and don't need to insure the building shell itself. BPP also covers improvements and betterments, which are the permanent upgrades you've made to a rented Dallas facility, such as custom flooring or specialized lighting that would remain if you vacated the premises.