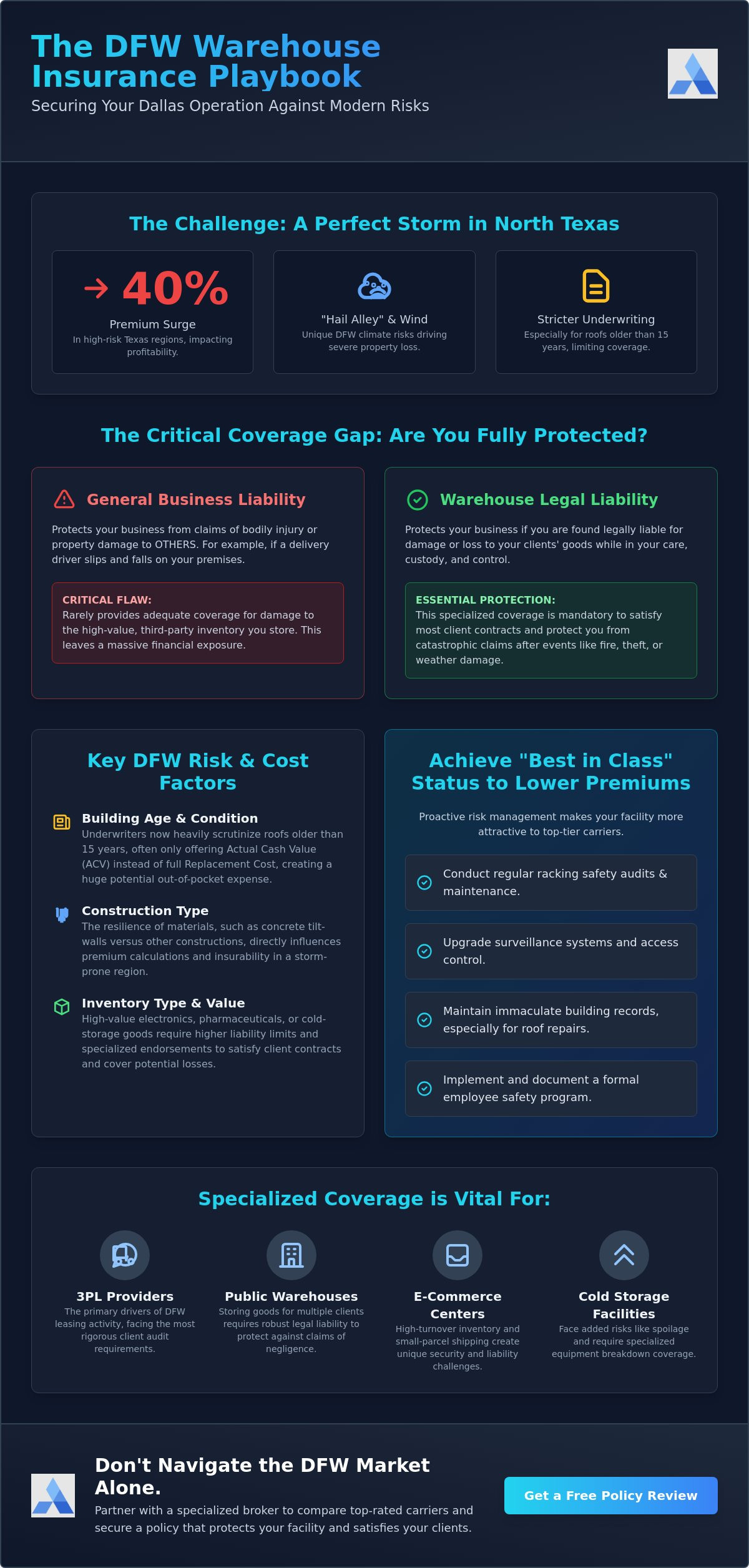

With commercial property insurance premiums in high-risk Texas regions surging by as much as 40% in recent years, many operators are finding that their coverage hasn't kept pace with the realities of 2026. You likely recognize the challenge of maintaining a profitable facility while meeting the rigorous insurance mandates required by global logistics partners. It's often frustrating to manage the technical gap between general liability and the specialized warehouse legal liability needed to protect high-value inventory against the region's notorious hail and wind events.

This guide helps you secure the specific warehouse insurance Dallas operations require to stay resilient against massive property loss and complex legal disputes. You'll learn how to navigate the latest market shifts, including the impact of Texas House Bill 2067 on policy renewals and the stricter underwriting standards now applied to commercial roofs older than 15 years. We'll examine how to structure a comprehensive system that satisfies client contracts, minimizes your out-of-pocket exposure for damaged goods, and ensures your facility remains a stable, protected link in the North Texas supply chain.

Warehouse insurance represents a sophisticated, multi-layered framework designed to safeguard both the physical structure and the immense value of goods moving through the region. In the Dallas-Fort Worth market, which currently manages approximately 1.12 billion square feet of industrial inventory, a standard commercial policy often falls short. Operators must distinguish between protecting their own assets and managing the liabilities associated with storing third-party inventory. This distinction is the foundation of warehouse insurance Dallas strategies, as it addresses the unique operational risks inherent in high-volume logistics. With the implementation of Texas House Bill 2067 in 2026, transparency in policy non-renewals has improved, yet the complexity of securing adequate limits remains a primary concern for local stakeholders.

The North Texas climate introduces specific challenges that differ significantly from coastal regions. While coastal areas focus on hurricanes, DFW operators face the persistent threat of "Hail Alley" and severe windstorms. These localized risks have contributed to commercial property insurance rate increases of up to 40% in high-risk zones. Understanding the nuances of Property insurance is essential for decision-makers who need to evaluate replacement cost versus actual cash value, especially as carriers implement stricter 2026 underwriting standards for aging roof systems.

To better understand the core components and costs associated with these policies, watch this helpful overview:

Dallas serves as a critical inland port, acting as a primary distribution hub for the entire Southwestern United States. Third-party logistics (3PL) providers here operate under higher liability standards than private storage facilities. These operators must adhere to specific legal obligations outlined in the Texas Business and Commerce Code, which governs the "duty of care" for warehouseers. Failure to maintain specialized coverage can lead to catastrophic out-of-pocket costs if inventory is damaged, as a standard Business Owners Policy (BOP) rarely provides the limits required by modern enterprise contracts.

The need for specialized warehouse insurance Dallas extends across various operational models. Public warehouse operators, who store goods for multiple clients, require robust legal liability to protect against claims of negligence. Cold storage facilities face additional technical hurdles, such as spoilage risks and equipment breakdown coverage for specialized refrigeration systems. Similarly, e-commerce fulfillment centers must manage high-turnover inventory challenges and the increased security risks associated with small-parcel shipping. Since 3PL firms are currently the major drivers of leasing activity in DFW, their insurance structures must be precise enough to satisfy the rigorous audit requirements of global retail partners.

Designing a robust risk management framework requires more than a generic policy. For operators in the DFW metroplex, the insurance structure must account for the high density of high-value inventory and the volatile local climate. Commercial Property Insurance serves as the first line of defense for the physical Dallas facility. In 2026, carriers have grown increasingly selective, often requiring updated appraisals to account for the 3% to 6% inflationary impact on property values. Furthermore, underwriters now scrutinize roof ages more than ever. Many insurers will only offer actual cash value settlements for roofs older than 15 years, making it vital to maintain the structural integrity of your building to avoid significant out-of-pocket loss during a claim.

General Liability Insurance is equally critical, addressing third-party bodily injury and property damage. While the Texas State Fire Marshal’s Office sets specific minimums for certain contractors, warehouse operators should aim for higher limits to protect against site accidents involving visitors or vendors. Adhering to OSHA warehouse safety standards not only protects your workforce but also signals to carriers that your operation is a lower risk, which can influence your premium tier. For goods that leave the facility, Inland Marine coverage bridges the gap, insuring inventory while it is in transit or stored temporarily at off-site locations.

A common point of confusion for new operators involves the "duty of care" for third-party goods. Standard property insurance typically only covers assets you own. Warehouse Legal Liability is the cornerstone of warehouse insurance Dallas programs for 3PL providers, as it covers your liability for damage to a customer's property due to your negligence. This is distinct from Bailee's coverage, which may pay regardless of fault. If a forklift operator accidentally punctures a pallet of high-value electronics, your legal liability coverage is what prevents a massive financial hit to your balance sheet. Consulting with an experienced team at amco.net can help you identify these specific policy triggers before a loss occurs.

North Texas weather events, particularly severe hailstorms, can halt operations for weeks. Business Interruption coverage is designed to replace lost income during these periods of forced inactivity. It's essential to ensure your policy includes an "actual loss sustained" clause, which provides more flexibility than fixed-limit coverage. Extra Expense coverage is also vital for logistics firms. It covers the costs of temporary relocation or expedited equipment rentals, ensuring you can meet client contracts even if your primary facility is undergoing repairs. Given that commercial property rates in high-risk Texas zones have increased by up to 40% recently, having a precise business continuity plan is no longer optional; it's a strategic necessity.

Underwriting a facility in North Texas requires a granular assessment of structural and environmental variables. While the average cost of a Business Owner's Policy in Texas sits around $877 annually for small firms, large-scale industrial operations face much higher premiums based on their specific risk profile. Carriers primarily look at the building's construction class. In the DFW market, concrete tilt-wall construction is the gold standard. It provides superior resistance to the extreme wind speeds common in North Texas compared to older metal-sided structures. If your facility features a roof older than 15 years, be prepared for stricter underwriting. Many carriers in 2026 are shifting these older systems to actual cash value settlements rather than replacement cost, significantly increasing your financial exposure during a loss.

The "Hail Alley" effect is perhaps the most significant localized driver for warehouse insurance Dallas pricing. Unlike coastal regions where hurricane risk dominates, North Texas experiences frequent, high-impact hailstorms. This volatility has led many insurers to implement separate wind and hail deductibles, often calculated as 1% to 2% of the total insured building value. Fire protection systems also play a pivotal role. Facilities equipped with Early Suppression, Fast Response (ESFR) sprinkler systems typically command better rates because they can control high-challenge fires without the need for in-rack sprinklers, reducing both fire and water damage risks.

Location within the DFW metroplex dictates more than just logistics efficiency. Proximity to professional fire departments and high-pressure hydrants in established industrial zones, such as the Great Southwest or the DFW Airport submarket, can lower your fire rating. Conversely, facilities in areas with higher reported crime rates may see increased premiums for theft and vandalism coverage. Security is no longer just a fence; carriers now look for "Best in Class" standards, including 24/7 monitored surveillance and restricted access controls, to offset these regional risks.

Your internal processes are just as important as the building's shell. High-pile storage, which involves stacking goods above 12 feet, triggers specific fire code requirements that insurers monitor closely. If you're storing hazardous materials or high-value consumer electronics, your risk profile intensifies due to either the potential for environmental catastrophe or the attraction for organized theft. Maintaining a comprehensive safety manual and documented employee training programs isn't just about compliance. It’s a financial strategy. A clean claims history is your most valuable asset; even a single major loss can lead to premium hikes of 10% to 40% that persist for years, making proactive risk mitigation essential for long-term cost stability.

Lowering your operational overhead requires a transition from reactive claims management to proactive operational excellence. While North Texas weather remains unpredictable, your facility’s internal environment is within your control. Carriers reward operators who demonstrate a commitment to "Best in Class" standards through documented safety protocols. Regular audits of racking systems and forklift operations are foundational. These inspections should verify that load capacities aren't exceeded and that safety pins are intact, reducing the likelihood of a catastrophic rack collapse. Documenting these audits provides the paper trail underwriters need to justify lower rate tiers.

Upgrading your surveillance and lighting systems also provides immediate underwriting benefits. Modern insurers look for 24/7 monitored video feeds and high-output LED lighting that eliminates blind spots in high-turnover zones. Implementing a strict visitor management policy at the loading dock is equally vital. By restricting access and documenting every individual entering the facility, you minimize the risk of theft and liability claims from unauthorized personnel. This level of control is particularly important for 3PL providers managing high-value consumer electronics or specialized equipment.

Your choice of building materials directly influences your warehouse insurance Dallas premiums. For instance, Thermoplastic Polyolefin (TPO) roofs are often preferred over traditional metal systems in North Texas due to their durability against hail impact and superior energy efficiency. Since many carriers in 2026 refuse to write new policies for roofs older than 15 to 20 years, investing in a replacement before the system reaches its limit is a strategic financial move. Additionally, installing smart water leak detection systems can prevent massive inventory loss from burst pipes, a common issue during Texas freeze events. These technological investments offer a clear ROI by qualifying your operation for premium credits and reducing your deductible exposure.

Protecting your balance sheet also involves shifting risk back to the parties best equipped to handle it. You should ensure that your client contracts require them to carry their own property insurance for the goods being stored. This practice, combined with robust hold-harmless agreements, limits your exposure to only those losses caused by your direct negligence. It's critical to review and update your inventory valuation methods annually to account for the 3% to 6% inflationary growth seen in 2026 property values. This ensures you aren't underinsured if a total loss occurs.

Managing these moving parts is complex, but you don't have to navigate it alone. You can request a comprehensive policy review to see which risk mitigation strategies will have the greatest impact on your specific premium structure. Always demand "Certificates of Insurance" from every vendor entering your site to ensure their liability doesn't become yours. This systematic approach to risk transfer ensures that your warehouse insurance Dallas policy remains a safety net rather than a primary source of funding for preventable losses.

AMCO.NET LLC brings over 35 years of specialized experience to the Texas commercial insurance market, providing a depth of knowledge that goes beyond standard policy issuance. As an independent broker, we don't represent a single carrier; we represent your business interests. This autonomy allows us to compare top-rated providers to find the specific warehouse insurance Dallas operators need to remain competitive and compliant in a tightening market. We understand that in the DFW logistics hub, your storage facility is often just one part of a larger, interconnected supply chain. Our team specializes in the seamless integration of warehouse coverage and commercial trucking insurance, ensuring there are no technical gaps in protection as inventory transitions from your loading dock to the highway.

The DFW logistics landscape is unique. It requires a partner who understands why a concrete tilt-wall facility near DFW Airport carries a different risk profile than a metal-sided structure in South Dallas. AMCO.NET LLC leverages our significant market history to advocate for your business, using your safety records and infrastructure upgrades to negotiate better terms with underwriters. This personalized approach ensures your coverage is a reflection of your operational excellence rather than a generic industry average.

Our role is to help Dallas businesses scale their coverage as they expand their footprint. Whether you are moving from a 50,000-square-foot facility to a 500,000-square-foot distribution center, your risk management needs will evolve. We possess the technical expertise required to combine commercial property insurance with complex liability structures, including specialized endorsements for cold storage or high-value electronics. When a claim occurs, you benefit from localized support. We understand the urgency of logistics and work to ensure that policy adjustments and claims processing don't become bottlenecks in your operations.

Evaluating your current risk profile is a straightforward process when you work with specialists. We analyze your facility's construction, fire suppression systems, and contractual obligations to build a comprehensive defense. It's a common industry trap to seek the lowest possible premium, but "cheap" insurance can be the most expensive mistake for a warehouse operator. Inadequate limits or missing legal liability endorsements can lead to millions in out-of-pocket costs after a single North Texas storm or forklift accident. AMCO.NET LLC focuses on value and long-term stability, ensuring your business is protected against the 10% to 40% rate increases currently impacting high-risk Texas zones. Protect your Dallas warehouse with an AMCO.NET LLC expert today and secure a policy that supports your growth and satisfies your most demanding logistics partners.

Maintaining a competitive edge in the Dallas-Fort Worth industrial market requires more than operational efficiency; it demands a sophisticated approach to risk management. As discussed, the volatility of the 2026 insurance landscape makes specialized coverage a strategic asset for any facility manager or 3PL provider. Securing the right warehouse insurance Dallas policy allows you to focus on scaling your logistics operations while ensuring your structure and the third-party inventory within are protected against the region's specific environmental and legal challenges.

AMCO.NET LLC has been serving Texas businesses since 1987, providing the technical expertise required to navigate high-risk commercial and trucking sectors. As an independent agency, we analyze your profile against multiple top-tier carriers to build a customized defense for your business. Get a Professional Warehouse Insurance Quote from AMCO.NET LLC to ensure your operation remains resilient, compliant, and ready for future growth in this vital inland port.

No, these coverages serve different functions. General liability addresses third-party bodily injury and property damage, such as a vendor slipping on your loading dock. Warehouse legal liability is specifically designed for 3PL providers to protect against claims for damage to a client's inventory that occurs due to your operational negligence.

Hail is typically a covered peril, but the deductible structure in Dallas is unique. Most policies now include a separate wind and hail deductible, often calculated as 1% or 2% of the total building value. This means you'll be responsible for a portion of the repair costs before your coverage begins to pay for the loss.

Bailee’s insurance provides coverage for damage to a customer’s property regardless of whether you were legally at fault. While warehouse insurance Dallas programs often center on legal liability, bailee’s coverage is a valuable addition for operators who want to maintain client relationships by paying for minor damages without a lengthy negligence investigation.

Premiums are highly individualized and depend on your facility's construction and safety systems. While a small Texas Business Owner's Policy might average around $877 annually, large distribution centers face much higher costs. Factors like a roof older than 15 years or the lack of an ESFR sprinkler system can significantly increase your annual premium.

Yes, standard commercial property policies exclude damage caused by rising surface water. Even if your facility is not in a high-risk zone, the flash flooding common during North Texas storms makes separate flood insurance a necessary protection. This ensures your building and your clients' goods are covered during extreme rain events.

Yes, AMCO.NET LLC specializes in creating integrated insurance portfolios for the logistics sector. We can bundle your warehouse insurance Dallas with commercial trucking and general liability coverage. This approach simplifies your administration and ensures there are no technical gaps in protection as inventory moves from your warehouse to your fleet.

Your legal liability coverage will typically respond if the theft occurred because you failed to maintain reasonable security. To provide broader protection, we recommend adding a crime endorsement. This protects against both external break-ins and internal employee dishonesty, which is critical for facilities handling high-value consumer electronics.

Spoilage is not covered under a standard policy and requires a specific rider. This endorsement covers the loss of perishable goods due to power outages or mechanical failure of refrigeration equipment. For Dallas operators, we often pair this with equipment breakdown coverage to manage the increased strain that Texas summers place on cooling systems.