If you think opting out of workers' compensation is a simple way to cut overhead in Texas, you might be overlooking a systemic risk that could dismantle your operation. Many owners find the process of securing business insurance quotes Austin requires to be fragmented and technically opaque, leading to either excessive premiums or dangerous gaps in protection. It's frustrating to manage high-growth assets while second-guessing if your liability limits align with the latest state mandates or city-specific contract requirements.

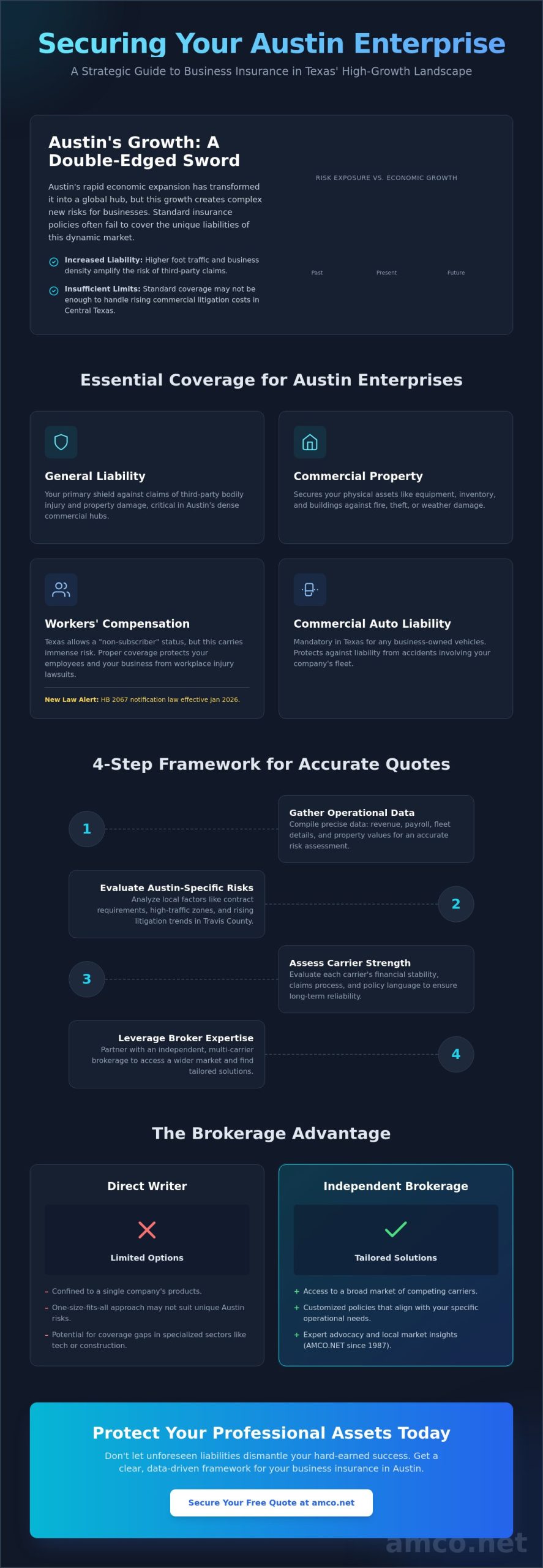

You deserve a clear, data-driven framework to protect your commercial interests. This guide explains how to secure accurate, cost-effective coverage tailored to the unique Austin market and Texas regulatory landscape. We will detail the critical differences between required and optional policies, including the implications of the new HB 2067 notification law effective January 2026. By the end of this analysis, you'll have a streamlined method to compare Texas carriers and the confidence that your professional assets are structurally sound against unforeseen liabilities.

Austin's transformation into a global economic powerhouse has fundamentally altered the risk environment for local enterprises. As business density increases across Travis County, the complexity of commercial liability grows in tandem. Obtaining business insurance quotes Austin owners can trust involves analyzing these local shifts rather than relying on national averages. A robust insurance strategy serves as a protective layer for your company's long-term valuation, ensuring that operational continuity remains intact even during unforeseen disruptions.

To better understand the nuances of commercial vehicle coverage and how it impacts your overall quote, watch this helpful video:

Investors and lenders in the Austin market view a comprehensive insurance portfolio as a sign of operational maturity. When you seek insurance quotes, lenders will often require specific surety bonds or high-limit liability coverage before approving capital. This isn't just about compliance; it's about ensuring that a single catastrophic event doesn't erase years of equity. Professional risk management transforms insurance from a recurring expense into a strategic asset that stabilizes your balance sheet and protects your professional reputation.

Retailers and service providers in the downtown corridor deal with significantly higher foot traffic than in previous years. This exposure increases the probability of third-party injury claims. Simultaneously, the rising cost of commercial litigation in Central Texas has made traditional liability limits insufficient for many mid-sized operations. If your business is expanding, your policy limits require frequent calibration. A standard Business Owner's Policy (BOP) provides a foundation, but it won't account for the unique operational risks of a high-growth market without professional customization and higher aggregate limits.

Choosing between a direct writer and an independent agency can determine the resilience of your business. Direct writers are limited to their own products, which may not offer the specific language needed for Austin's unique construction or tech sectors. AMCO.NET LLC has been operating since 1987, providing a level of local context that newer, digital-only platforms lack. This tenure allows for a more nuanced interpretation of market trends and carrier reliability. By evaluating business insurance quotes Austin through a multi-carrier brokerage, you access a broader range of underwriting appetites and pricing structures. A local advocate is indispensable during the claims process, ensuring technical details are handled with precision and professional distance.

Focusing on the technical architecture of your risk management strategy is essential for long term stability. While the previous section highlighted the broader economic climate, this section details the specific policy components that form a resilient defense for your company. Obtaining business insurance quotes Austin agencies provide requires a granular understanding of which coverages align with your specific industry vertical and physical location.

General Liability serves as the primary shield against common operational risks. It addresses claims involving third-party bodily injury and property damage, which are increasingly common in Austin’s dense commercial hubs. It’s vital to recognize that this policy does not cover everything; professional errors and employee-related claims require separate endorsements. For those maintaining a physical presence in high-rent districts like The Domain or East Austin, Commercial Property Insurance is non-negotiable. It secures your investment in specialized equipment, inventory, and tenant improvements against fire, theft, or wind damage. Small to mid-sized enterprises often find that a Business Owner’s Policy (BOP) offers the most efficient structure. This package combines liability and property protection into one manageable policy, often at a lower premium than separate contracts. The SBA guide to business insurance provides a helpful framework for understanding these foundational requirements at a high level before you customize for the Texas market.

Austin’s professional services and technology sectors face intangible risks that physical property policies ignore. Professional Liability, or Errors and Omissions (E&O), is critical for anyone providing expert advice, legal services, or technical solutions. If a software bug or a consulting error leads to a client's financial loss, E&O is the only policy that manages the resulting legal defense and settlement costs. Similarly, Cyber Liability has become a prerequisite for Austin’s SaaS firms and digital startups. This coverage handles the fallout from data breaches, including forensic investigations, credit monitoring for affected parties, and regulatory fines. When evaluating business insurance quotes Austin tech firms should prioritize carriers with robust cyber response teams. Combining these specialized coverages into a single portfolio not only simplifies administration but often results in more favorable pricing models. For a technical audit of your current coverage gaps, reaching out to a specialist at amco.net can help ensure your digital and professional assets are fully accounted for.

Operating a business in Central Texas requires a precise understanding of state-level mandates and localized municipal requirements. Whether your headquarters are in the Travis County tech corridor or you're managing construction projects in Williamson County, compliance is a prerequisite for professional credibility. Aligning your operation with Texas commercial insurance guidelines ensures that you don't just meet the minimum legal threshold but also protect your equity from statutory liabilities. When requesting business insurance quotes Austin providers generate, you must account for these specific regulatory layers to avoid coverage gaps that could trigger legal penalties or contract forfeitures.

Texas remains unique as a "non-subscriber" state, meaning private employers aren't strictly required by law to carry Workers' Compensation insurance. However, this flexibility introduces a significant systemic risk. Businesses that opt out lose their common-law defenses in employee injury lawsuits, potentially facing unlimited liability for medical costs and lost wages. In the Austin market, most commercial landlords and municipal contracts mandate proof of Workers' Comp regardless of state law. Maintaining this coverage protects the employer's assets from litigation as much as it provides for the employee's recovery. It's a foundational component of a stable risk management system that prevents a single workplace accident from becoming a terminal financial event.

Beyond vehicle and injury protection, Austin contractors must navigate specific surety bond requirements. For example, insurance agencies in the city require a $25,000 surety bond, while notaries public must maintain a $10,000 bond. Furthermore, the implementation of HB 2067 on January 1, 2026, adds a new layer of transparency to the market. This law requires insurers to provide written explanations for policy cancellations or non-renewals. This regulatory shift makes it easier for Austin business owners to understand their risk profile and address the underlying reasons for premium adjustments or coverage changes. When you evaluate business insurance quotes Austin carriers provide, ensure they've accounted for these 2026 compliance standards to maintain uninterrupted operational status.

Securing a reliable commercial policy requires more than just a cursory search for the lowest price. While many national platforms prioritize a rapid speed-to-quote model, this haste often results in classification errors that trigger expensive premium audits at the end of the policy term. Obtaining the business insurance quotes Austin enterprises need for long-term stability demands a methodical approach to data collection. Accuracy at the application stage ensures that the price you're quoted remains the price you pay, protecting your cash flow from unexpected adjustments.

Professional risk management involves a technical evaluation of your operational metrics. When you provide precise revenue and payroll projections, you're not just filling out a form. You're defining the exposure levels that underwriters use to calculate your risk. Underestimating these figures might lower your initial premium, but it creates a liability during the annual audit process where carriers can bill you for the discrepancy. Conversely, overestimating these figures ties up capital that could be better deployed into your Austin operations. Balance is essential for financial efficiency.

Before initiating the quote process, organize your technical documentation to ensure consistency across different carrier submissions. You will need your Federal Tax ID (FEIN), the exact legal name of your entity, and a detailed description of your operations. Underwriters look for specific risk markers, so defining your scope of work with precision prevents you from being placed in a high-risk category that doesn't apply to your business. Most importantly, you must provide loss runs for the past 3 to 5 years. These official reports from your previous carriers document your claims history and serve as the primary evidence of your company's safety record and risk profile.

A comprehensive comparison of business insurance quotes Austin providers offer must extend beyond the monthly premium. You should carefully evaluate the "sweet spot" between your deductible and your premium. A higher deductible can significantly reduce your fixed costs, but it requires enough liquid capital to cover out-of-pocket expenses if a claim occurs. Additionally, you must understand the difference between "Claims-Made" and "Occurrence" policy forms. An occurrence policy covers incidents that happen during the policy period regardless of when the claim is filed, while a claims-made policy only covers claims filed while the policy is active. This distinction is critical for long-tail liabilities in sectors like construction or professional consulting. To ensure your data is analyzed by an expert rather than an algorithm, you can request a professional quote review to identify potential gaps in these technical variables.

Choosing a strategic partner for your risk management is as critical as the coverage itself. In a market as volatile as Central Texas, relying on a transactional vendor often leads to technical gaps in your defense. AMCO.NET LLC operates on a foundation of deep professionalism and B2B expertise, ensuring that business insurance quotes Austin companies receive are grounded in operational reality rather than algorithmic guesswork. We position ourselves as consultants who understand the systemic needs of your business, from commercial property protection to complex surety bond requirements.

The primary advantage of our approach lies in our independent brokerage model. While direct writers are restricted to their own proprietary products, we leverage a diverse panel of highly rated carriers to find the most efficient path for your specific industry. This multi-carrier perspective allows us to identify the "sweet spot" between premium costs and comprehensive liability limits. It's a level of customization that online-only platforms cannot match, especially when dealing with the nuanced regulatory environment of Travis and Williamson counties.

Since our founding in 1987, we've focused on delivering stable, long-term solutions for Texas enterprises. We understand that modern business owners require both professional depth and technological efficiency. To support this, we manage policies through a dedicated mobile application, allowing you to access certificates of insurance and policy details with precision. This balance of traditional expertise and digital convenience ensures your operational continuity is never compromised by administrative delays. For those managing assets across the state, our Comprehensive Guide to Insurance in Houston provides additional insights into the broader Texas commercial landscape.

Securing your company's future starts with a technical audit of your current exposure. You can initiate this process by requesting business insurance quotes Austin through our secure online portal. Once we've analyzed your data, a licensed Texas agent will be available to discuss the specific variables of your quote, ensuring every industry-specific risk is addressed. This consultation isn't a sales pitch; it's a professional evaluation of your company's resilience. We invite you to secure your Austin business with a professional quote from AMCO.NET LLC today and experience the stability that comes from nearly four decades of Texas insurance expertise.

The technical architecture of your risk management strategy determines your company's resilience in the high-velocity Travis County market. As we've analyzed, moving beyond basic coverage to a system that accounts for Texas-specific workers' comp nuances and 2026 regulatory updates is vital. Relying on accurate data during the application phase ensures that the business insurance quotes Austin enterprises receive are both stable and audit-proof. By leveraging a multi-carrier brokerage model, you gain access to the specialized underwriting appetites of top-rated national and regional carriers.

AMCO.NET LLC has been serving Texas businesses since 1987, providing the professional distance and expert advocacy needed to manage complex claims. Our mobile application allows for seamless policy management, ensuring your certificates of insurance are always accessible when contract opportunities arise. Don't leave your company's valuation to chance in a competitive landscape. Get Your Free Austin Business Insurance Quote Today and establish a foundation of professional security. We look forward to supporting your long-term growth and operational stability.

Texas law mandates commercial auto insurance for all business-owned vehicles, but most other coverages are not strictly required by state statute. However, the City of Austin frequently imposes specific insurance requirements for contractors and event organizers. For instance, contracting with city venues often requires a minimum of $1 million per occurrence in general liability coverage. This ensures that your business meets the professional safety standards necessary for local government partnerships.

The cost of a general liability policy depends on several technical factors, including your industry classification, annual revenue projections, and payroll size. While market averages exist, your specific risk profile in the Austin area will ultimately determine the premium. Factors such as high foot traffic in retail locations or specialized professional services in the tech sector can lead to variations in the quotes provided by different carriers during the underwriting process.

A Business Owner's Policy (BOP) is a bundled insurance package that combines general liability and commercial property insurance into a single contract. While general liability focuses on third-party bodily injury and property damage claims, a BOP extends protection to your company's physical assets, such as equipment and inventory. This consolidated structure often provides a more cost-effective solution for small to mid-sized enterprises than purchasing individual policies separately from multiple providers.

Texas law does not strictly require private employers to carry workers' compensation insurance, regardless of whether you have one employee or many. However, choosing to operate as a non-subscriber exposes your business to unlimited legal liability if an employee is injured on the job. Without this coverage, you lose important common-law defenses in court, making it a critical consideration for protecting your company's long-term financial health and operational stability.

Yes, AMCO.NET provides a dedicated mobile application designed for efficient policy management and document access. This tool allows you to view your insurance documents, check policy details, and manage certificates of insurance directly from your smartphone. This technological integration ensures that you have the necessary documentation ready for client meetings or contract signings without the delays associated with traditional paper-based systems or manual office requests.

The timeline for receiving business insurance quotes Austin providers generate varies based on the complexity of your operations. While basic liability policies for low-risk industries can often be processed quickly, more specialized sectors like construction or technology may require a deeper underwriting review. A consultative approach typically takes between one and three business days to ensure that all industry-specific risks are accurately assessed and documented for a reliable final quote.

To secure an accurate quote, you must provide your Federal Tax ID (FEIN), legal business name, and detailed revenue and payroll projections. You should also have your claims history, known as loss runs, available for the past three to five years. Providing this granular data helps underwriters categorize your risk correctly, which prevents future premium adjustments and ensures the business insurance quotes Austin carriers provide are technically sound and audit-ready.

Yes, AMCO.NET provides various surety bonds required for professional compliance and municipal contracting in the Austin area. This includes the $25,000 bond required for insurance agencies and the $10,000 bond necessary for notaries public. Contractors working on city projects often need performance or payment bonds to meet specific local requirements. Our team assists in identifying the specific bond types and limits required for your particular trade or city contract.