Securing affordable car insurance for a 17 year old in Houston often feels like an impossible balancing act between astronomical premiums and the necessity of robust protection. You're likely facing significant sticker shock as you analyze the current market, especially since Houston's congested corridors and high accident rates naturally elevate local risk profiles. It's a common frustration for parents who want to ensure their child's safety while maintaining a disciplined, professional approach to their household's financial commitments.

This 2026 guide provides a structured framework for navigating Texas-specific regulations, including the mandatory 30/60/25 liability limits and the operational requirements of the Graduated Driver's License program. We'll examine how to optimize your coverage through strategic discounts for academic performance and telematics, while explaining why integrating a teen into an existing family policy is typically the most economically viable path. You'll gain the expert insight needed to secure a policy that balances cost efficiency with the comprehensive liability protection required for the unique driving environment of the Houston metropolitan area.

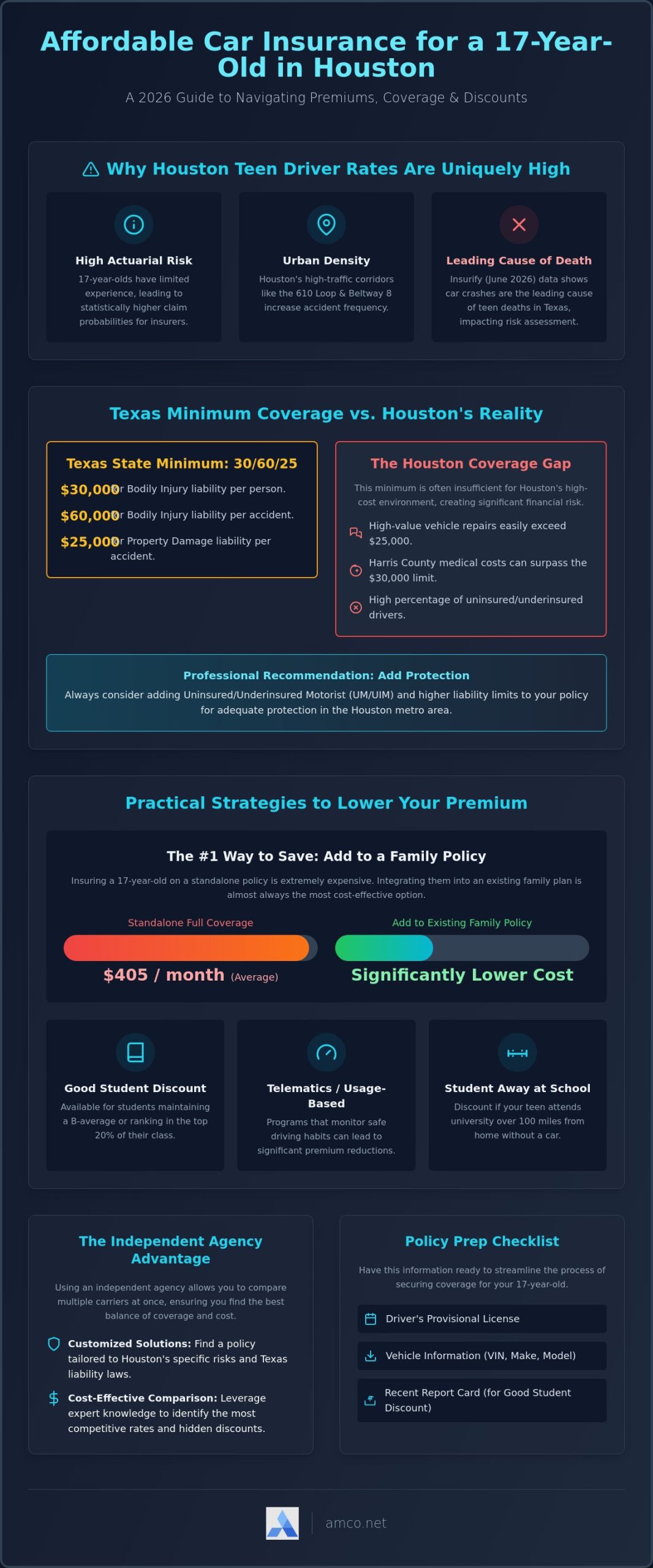

Actuarial risk assessment is a cold calculation of probability. For a 17-year-old, the probability of a claim is statistically higher due to limited behind-the-wheel experience. In Texas, insurance carriers use these metrics to determine premiums, focusing heavily on the transition from a learner's permit to a provisional license. This age is a critical threshold where a driver's exposure to traffic increases significantly, leading to higher financial risks for the insurer.

Understanding how Vehicle insurance in the United States is structured helps clarify why local variables are so influential. The Texas Department of Insurance oversees rate filings to ensure they remain fair, but the agency doesn't set the prices. Instead, local claim history and urban density dictate the final cost of car insurance for a 17 year old in Houston. Carriers view the metropolitan area as a high-frequency environment where accidents are more likely than in rural counties.

To better understand how to manage these costs, watch this helpful video:

Texas law mandates a minimum liability coverage of 30/60/25. This provides $30,000 for bodily injury per person, $60,000 per accident, and $25,000 for property damage. While this meets the legal threshold, it's often insufficient for the Houston environment. A single collision involving a high-value vehicle on the West Loop can easily exceed $25,000 in repairs. Medical costs in Harris County also frequently surpass the $30,000 per-person limit, leaving families vulnerable to personal litigation. Professional advisors often recommend Uninsured/Underinsured Motorist (UM/UIM) coverage, as Harris County maintains a high percentage of drivers operating without valid policies.

Urban density is a primary driver of premiums in the region. Local infrastructure, such as the Grand Parkway and Beltway 8, involves high-speed merging and complex traffic patterns that challenge inexperienced operators. According to Insurify (June 2026), car crashes remain the leading cause of teen deaths in Texas. This data forces carriers to categorize Houston as a high-risk territory. When you seek car insurance for a 17 year old in Houston, the premium reflects the reality of navigating the fourth-largest city in the country. The frequency of fender benders and multi-car pileups in dense urban corridors creates a risk profile that rural territories simply don't share.

Managing the financial impact of car insurance for a 17 year old in Houston requires a methodical approach to available credits and policy architecture. Carriers often provide significant premium offsets for drivers who demonstrate lower risk profiles through academic achievement or formalized training. This isn't just a marketing incentive; it's a data-driven response to the fact that responsible behavior in other areas of life often correlates with safer driving habits.

Texas insurers typically offer a "Good Student Discount" for those maintaining a B-average or ranking in the top 20% of their class. In 2026, many carriers have updated these requirements to include verification from technology-integrated driver training programs. These advanced courses go beyond the basics, focusing on urban hazard perception specific to dense environments like Harris County. Additionally, if your teen attends a Texas university more than 100 miles from home without a vehicle, the "Student Away at School" rule can significantly lower your costs.

Data from Insurify (June 2026) indicates that adding a teen to a family policy is almost always more economical than a standalone plan. While a standalone full-coverage policy averages $405 per month, adding a driver to an existing policy typically results in a monthly increase of $304. You can optimize these figures by bundling your auto coverage with Homeowners Insurance. This multi-policy approach creates a system-wide discount that stabilizes the overall household insurance budget.

Telematics and usage-based insurance (UBI) programs represent another professional tool for cost control. These apps monitor braking, speed, and nighttime driving, providing real-time data that can lead to tiered discounts. The Insurance Institute for Highway Safety highlights that vehicle choice also plays a decisive role in premium calculations. Securing cost-effective car insurance for a 17 year old in Houston depends heavily on selecting a vehicle with high safety ratings and moderate engine power, which reduces the actuarial risk.

Adjusting deductibles can lower premiums, but this requires a careful assessment of your liquid reserves. If you increase a collision deductible from $500 to $1,000, you're essentially self-insuring that first $1,000 of risk. For many Houston families, this trade-off makes sense when paired with the safety net of a comprehensive policy. You might find it beneficial to compare current market rates with an independent agent to see which combination of discounts and structures yields the highest ROI for your specific situation.

The infrastructure of Houston presents unique operational challenges that standard insurance definitions often fail to address adequately. While basic liability meets legal mandates, the high-velocity environment of the 610 Loop and the unpredictability of Gulf Coast weather patterns require a more sophisticated coverage layer. For a 17-year-old with limited experience, these local variables aren't just theoretical risks; they're daily operational hazards that demand a proactive insurance strategy. Transitioning from suburban streets to major interchanges like I-45 requires a policy that accounts for higher accident frequency and severity.

Houston's susceptibility to sudden flash flooding makes comprehensive coverage a necessity rather than an optional add-on. Even a stationary vehicle can suffer a total loss during a severe storm or tropical depression, events that occur with regularity in Southeast Texas. Collision coverage is equally vital, especially when navigating the dense traffic of the 610 Loop where fender benders are statistically more likely. These aren't just minor incidents; they're events that can lead to significant financial disruptions if the policy isn't structured to handle the actual cost of repairs in the current market.

Texas law requires insurers to offer Personal Injury Protection (PIP) unless it's waived in writing. PIP provides a critical buffer for medical expenses regardless of fault, offering a layer of security that standard Medical Payments coverage doesn't match because it also covers lost wages and non-medical costs. We also recommend integrating roadside assistance into the policy. For an inexperienced driver, a mechanical failure or a flat tire on a busy Houston freeway is a safety crisis, not just an inconvenience. Having a professional recovery system in place ensures the driver's safety while protecting the vehicle from further damage.

Harris County consistently reports high rates of drivers operating without valid insurance. When you secure car insurance for a 17 year old in Houston, Uninsured/Underinsured Motorist (UM/UIM) coverage is perhaps the most important technical addition. It bridges the gap when your teen is involved in an accident with a party who lacks sufficient limits or has no coverage at all. This protection extends to both bodily injury and property damage, ensuring that a third party's lack of compliance doesn't result in a total financial loss for your family. It's a vital safety net in an urban environment where compliance with state insurance mandates is inconsistent.

Moving beyond the Texas state minimums is essential for long-term asset protection. We advise a 100/300/100 structure, which provides $100,000 per person for bodily injury, $300,000 per accident, and $100,000 for property damage. The cost-to-value ratio for these higher limits is surprisingly favorable when compared to the risk of personal litigation following a major accident. It protects the household's stability from the legal risks inherent in complex collisions. AMCO.NET LLC plays a critical role here, helping to calibrate these limits based on your total household risk. This ensures the car insurance for a 17 year old in Houston integrates seamlessly with your broader financial security strategy, shielding your assets from the unpredictable nature of urban traffic incidents.

Direct-to-consumer insurance platforms often prioritize transaction speed over technical accuracy. While an automated quote might seem efficient, it lacks the nuanced risk assessment required for car insurance for a 17 year old in Houston. Independent agencies operate on a multi-carrier platform, allowing for a comprehensive market comparison that a single-brand insurer cannot replicate. This structural advantage ensures that you aren't just buying a product; you're implementing a tailored risk management solution. AMCO.NET LLC facilitates this by analyzing the specific risk profiles of various carriers to find the optimal fit for your household.

AMCO.NET LLC has maintained a consistent presence in the Houston market for 39 years. This tenure provides us with a deep understanding of Harris County court trends and local claim behaviors. Understanding how local juries view liability or how specific regional adjusters handle claims allows us to provide more accurate advice than a national call center. It's the difference between a generic policy and one calibrated for the specific legal and operational environment of Southeast Texas. Our system-level approach focuses on long-term stability rather than short-term price fluctuations, ensuring your coverage remains robust as market conditions evolve.

Brokers have the professional capacity to access specialized carriers that focus on younger demographic risk pools. If a violation occurs, we can assist in navigating the complexities of SR-22 insurance Texas requirements without the policyholder losing their primary coverage. As the driver gains experience and their risk profile improves, we can pivot the policy to more competitive carriers. This flexibility is impossible with direct insurers, where a single incident might result in a non-renewal or a significant premium spike that lasts for years. AMCO.NET LLC manages this transition as a strategic partner, protecting your insurability over time.

A professional risk assessment identifies coverage gaps that automated systems frequently overlook. When securing car insurance for a 17 year old in Houston, we look at the total household risk, not just the individual vehicle. This long-term management ensures a smooth transition as the driver moves into adulthood and their insurance needs evolve. Automated quotes can't account for the long-term financial goals or the specific asset protection needs of a Houston family. You can request a professional policy review with AMCO.NET LLC to ensure your current coverage aligns with these technical requirements and your family's financial security.

The transition from policy selection to formal issuance requires a methodical verification of data. Finalizing car insurance for a 17 year old in Houston is a process defined by precision, ensuring that the coverage limits and discounts discussed in previous sections are accurately reflected in the final contract. This administrative phase is the foundation of your long-term relationship with your carrier and agency, providing the legal certainty required for Texas road operations.

The timeline for binding coverage is typically efficient. Once we receive and verify all necessary documentation, AMCO.NET LLC can often issue a policy binder within 24 to 48 hours. This allows for immediate legal compliance, which is essential for meeting Texas Department of Public Safety requirements. You should be prepared to provide the first month's premium at the time of binding to ensure there are no gaps in protection during the policy's inception. This initial payment activates the contractual obligations of the carrier, securing your financial interests immediately.

To initiate a formal quote, you'll need to provide several key data points. This includes the Vehicle Identification Number (VIN) for each car, driver's license numbers for all household members, and the academic records required for the Good Student Discount. For those managing multiple responsibilities, our mobile app provides a streamlined platform for uploading these documents and managing your policy in real-time. Finalizing your car insurance houston quote with an agent ensures that every technical detail, from liability limits to deductible structures, is optimized for your specific risk profile.

Policy issuance is only the beginning of our professional support. If your teen is involved in an accident within the Houston metropolitan area, the immediate priority is safety and data collection. Our local office serves as your primary advocate, managing communication with the insurance carrier and ensuring the claims process adheres to professional standards. We understand the stress these incidents cause. Our role is to provide a calm, expert presence that facilitates a fair resolution. You can contact AMCO.NET LLC directly for immediate assistance, bypassing national call centers for a more personalized, expert response.

We recommend a full policy reassessment every six months. As a 17-year-old gains experience and potentially reaches new academic milestones, their actuarial risk profile shifts. Regular reviews allow us to pivot your car insurance for a 17 year old in Houston to reflect these improvements, potentially unlocking lower rates or more comprehensive coverage options. This proactive management ensures your household's insurance system remains both cost-effective and structurally sound as your driver transitions into adulthood.

Managing the complexities of car insurance for a 17 year old in Houston requires a proactive and informed approach. You've seen that while Texas mandates basic liability, the urban density of Harris County necessitates a more robust framework. By leveraging educational discounts and selecting an independent agency, you can balance cost efficiency with the high liability limits needed to protect your household's financial future. Our approach focuses on long-term stability rather than short-term fixes, ensuring your driver has the right support at every milestone.

AMCO has been serving Houston drivers since 1987, providing the local expertise and professional advocacy required to navigate Texas insurance law. We offer access to multiple A-rated insurance carriers, allowing us to build a customized system that meets your specific needs. Don't leave your family's security to chance in Houston's high-traffic environment. Get a fast and affordable Houston car insurance quote from AMCO today and ensure your teen driver has the reliable protection they deserve as they take to the road. We look forward to helping you secure a policy that brings peace of mind to your entire family.

Yes, adding a teen to a family policy is almost always more cost-effective than purchasing a standalone plan. While individual policies for young drivers carry high premiums due to their lack of experience, family plans allow the risk to be spread across multiple drivers and vehicles. This structure usually results in a lower per-driver cost than a separate policy would require.

The cost varies significantly based on the coverage type and the specific metropolitan area. Drivers in high-density regions like Harris County typically face higher premiums than those in rural parts of the state. Rates are influenced by factors such as the vehicle's safety rating, the driver's academic standing, and whether the policy includes full coverage or just the state-mandated liability limits.

No, they don't need a separate policy, but they must be officially listed as a driver on your existing coverage. Texas insurance regulations require that all licensed household members be disclosed to the carrier. Failing to list an occasional driver can lead to a claim denial if an accident occurs while they're operating the vehicle.

Yes, a 17-year-old can obtain an individual policy, but it's often difficult because minors cannot legally enter into binding contracts. Most carriers require a parent or guardian to co-sign the agreement. It's also important to note that standalone car insurance for a 17 year old in Houston is generally the most expensive way to secure coverage.

The most common incentives include the Good Student Discount for maintaining a B average and credits for completing state-approved driver education courses. Many insurers also offer telematics programs that monitor driving habits through a mobile app. These programs provide data-driven discounts for safe behaviors like avoiding hard braking and staying off the road during late-night hours.

A single moving violation can lead to a substantial premium increase for a young driver. Because 17-year-olds are already in a high-risk actuarial pool, carriers view a speeding ticket as a sign of increased liability. It can also cause the driver to lose "safe driver" or "accident-free" discounts, which compounds the total financial impact on the household policy.

Texas law only requires the state minimum liability limits of 30/60/25. However, if the teen's vehicle is financed or leased, the lienholder will require full coverage, including collision and comprehensive. Even without a loan, professionals recommend higher limits when securing car insurance for a 17 year old in Houston to protect against the high costs of urban accidents.

Focus on vehicle selection and academic performance to offset the higher statistical risk associated with young male drivers. Choosing a four-door sedan with a high safety rating rather than a high-performance vehicle can lead to lower premiums. Encouraging the completion of advanced safety courses also provides carriers with the data they need to justify a rate reduction.